NO.PZ2016071602000011

问题如下:

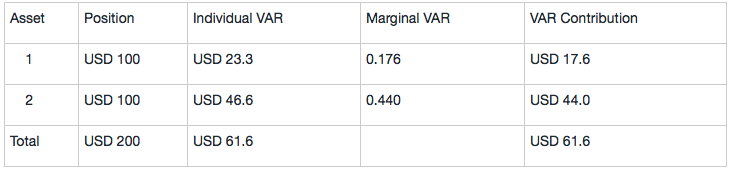

A risk manager assumes that the joint distribution of returns is multivariate normal and calculates the following risk measures for a two-asset portfolio:

If asset 2 is dropped from the portfolio, what is the reduction in portfolio VAR?

选项:

A. USD 15.0

B. USD 38.3

C. USD 44.0

D. USD 46.6

解释:

B is correct. This is 61.6 minus the portfolio VAR of asset 1 alone, which is USD 23.3, for a difference of 38.3.

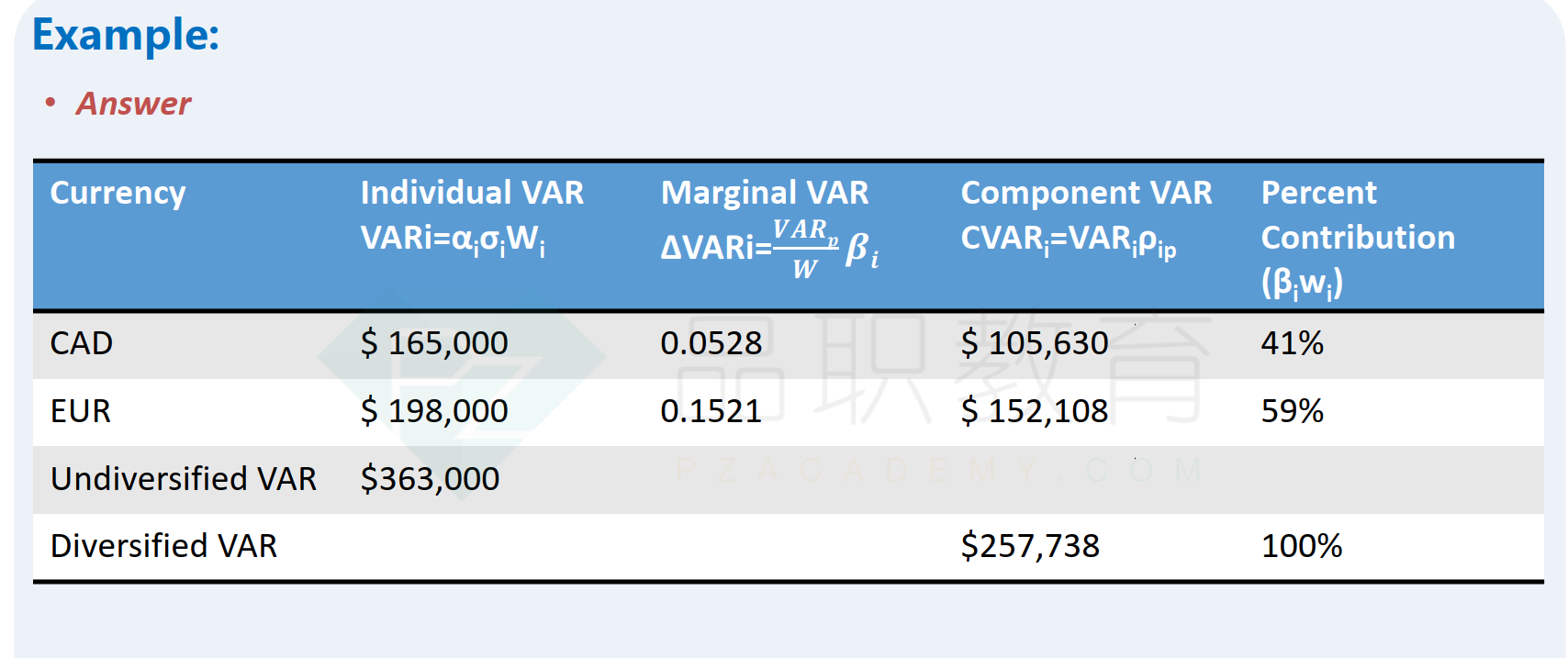

1.老师说求的是incremental var,那为啥用marginal var 乘以变动的100块钱得不出答案呢 2.individual vat是component var吗 3.var contribution是啥,对应讲义里讲的哪个名词,又是怎么计算出来的呢