CFA官网Practice题目:Alternative Investments for Portfolio Management

Raritan Case Scenario

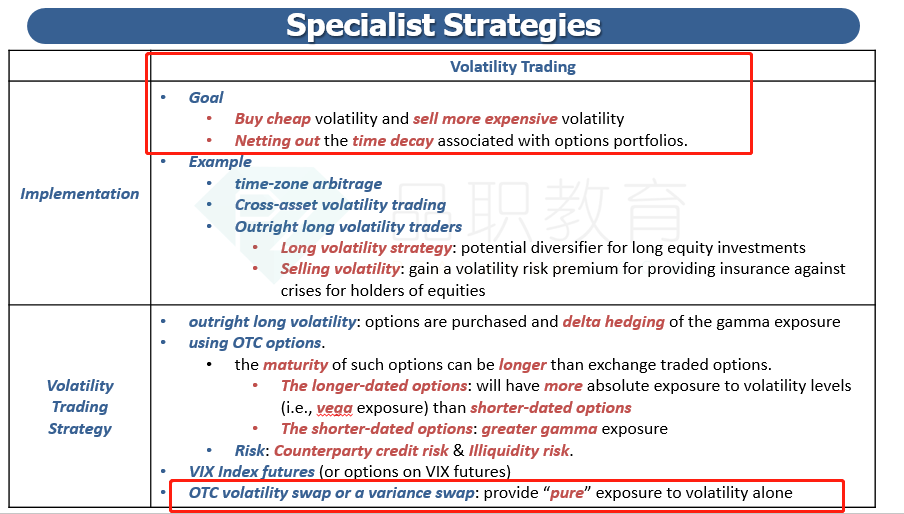

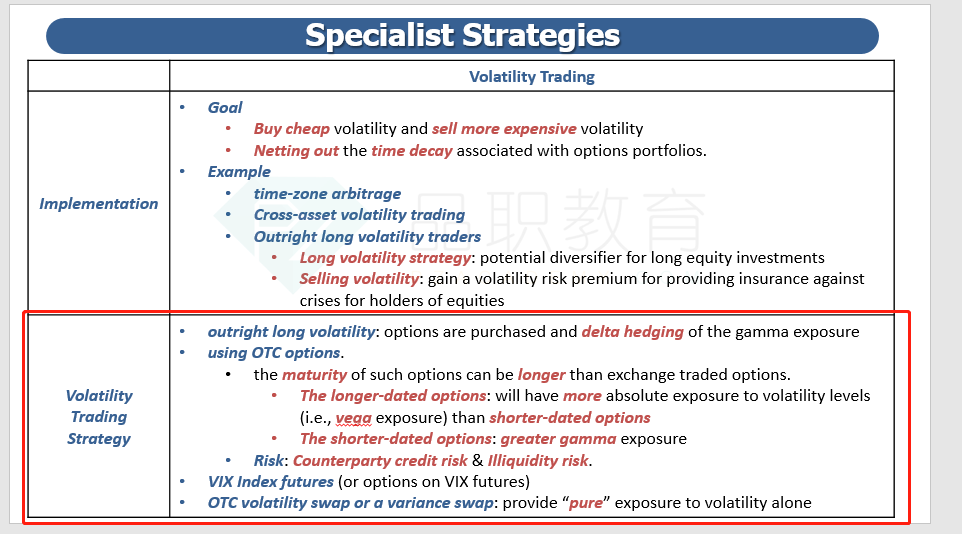

Rivas moves on to a specialist hedge fund strategy that focuses exclusively on volatility trading. Adding this fund to an investor’s portfolio strives to hedge long equity positions. The Taurus Fund typically implements the following three trades in its strategy:

Trade 1: Sell exchange-traded and over-the-counter equity call options on a market index. Selection of the options depends on the volatility smile and skew.

Trade 2: Sell VIX futures to capture the volatility premium and roll-down payoff.

Trade 3: Purchase a receiver volatility swap with an at-inception fair value of zero.

Which of the trades undertaken by the Taurus Fund is most likely to accomplish the objective that Rivas sets as the reason for considering the strategy?

A.Trade 1

B.Trade 2

C.Trade 3

Solution

C is correct. Equities and volatility are negatively correlated. In order to hedge the equity exposure in the portfolio, a long volatility position is necessary. Trade 1, a short volatility position, will not hedge the equity position since a long volatility position is needed. Trade 2 is also a short position in volatility; the intent is to collect a premium for selling volatility. This trade will sell off at the same time as equities are selling off and, therefore, provide a hedge. Trade 3 is an outright purchase of volatility via a swap, which provides a pure long exposure and would hedge the existing equity exposure in the portfolio.

看不懂答案的解释,1.为什么需要buy volatility?原本long stock已经有volalatility了,为什么还要增加? 2.Trade 1,3的做法如何理解?谢谢!