NO.PZ2018123101000091

问题如下:

Note: Each bond has a remaining maturity of three years, annual coupon payments, and a credit rating of BBB.

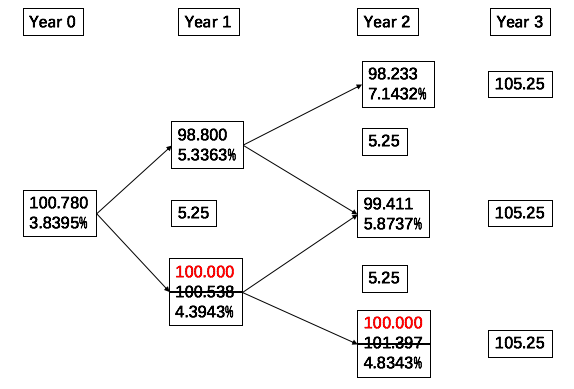

Bianchi constructs binomial interest rate tree based on a 10% interest rate volatility assumption and a current one-year rate of 1%. Panel A of Exhibit 2 provides an interest rate tree assuming the benchmark yield curve shifts down by 30 bps. Panel B provides an interest rate tree assuming the benchmark yield curve shifts up by 30 bps.

Bianchi determines that the AI bond is currently trading at an option-adjusted spread (OAS) of 13.95 bps relative to the benchmark yield curve.

Based on Exhibits 1 and 2, the effective duration for the AI bond is closest to:

选项:

A.1.98.

B.2.15

C.2.73

解释:

B is correct.

考点:考察Effective duration的计算

解析:

本题的计算比较多,需要利用利率向上平移的二叉树计算出PV(+),并且利用利率向下平移的二叉树计算出PV(-)。PV0为100.200为表一中已知信息。

利率向下平移30 bps,债券价格 (PV – ) 为100.78.

利率向上平移30 bps,债券价格(PV+) 为99.487.

利用Effective duration公式有:

该题二叉树计算过程是105.25向T0方向进行推导计算V+和V-,那算出来的是合理定价。在计算的过程中,一直对这个100.2是否为V0存疑。如何判断100.2就是合理定价?