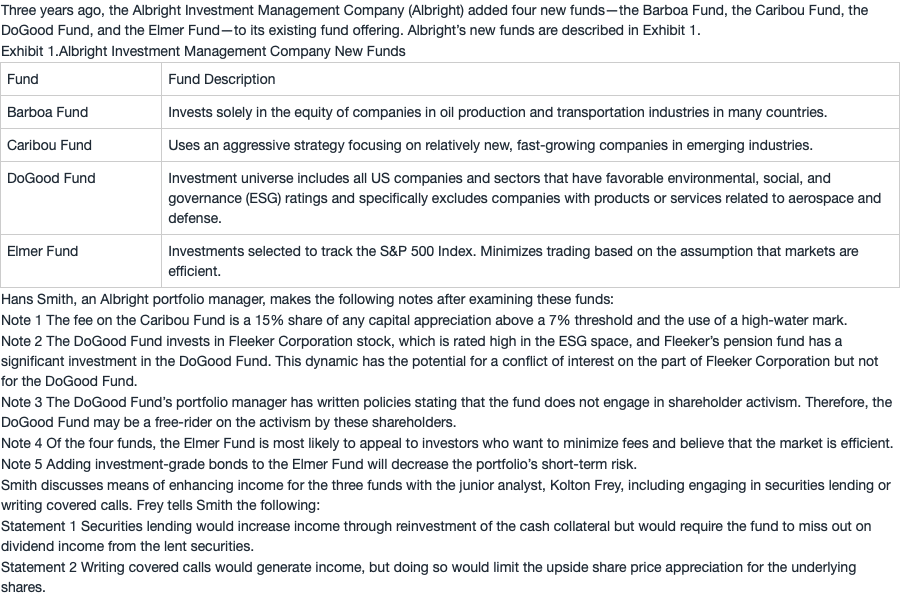

NO.PZ201809170400000107

问题如下:

Which of the notes regarding the Elmer Fund is correct?

选项:

A.Only Note 4

B.Only Note 5

C.Both Note 4 and Note 5

解释:

A is correct. For passively managed portfolios, management fees are typically low because of lower direct costs of research and portfolio management relative to actively managed portfolios. Therefore, Note 4 is correct.

Note 5 is incorrect because the predictability of correlations is uncertain.

这题我觉得出的不大好啊?也没讲是金融危机的条件下,如果讲了那肯定是基本所有资产类型的correlation都得上升。

按照另类里学的知识我记得好像是短期diversification加入Bond,长期diversification加入alternative资产,这样分散化才好。 特别是这题讲了降低short term risk,很容易联想到那个知识点。