NO.PZ201702190300000401

问题如下:

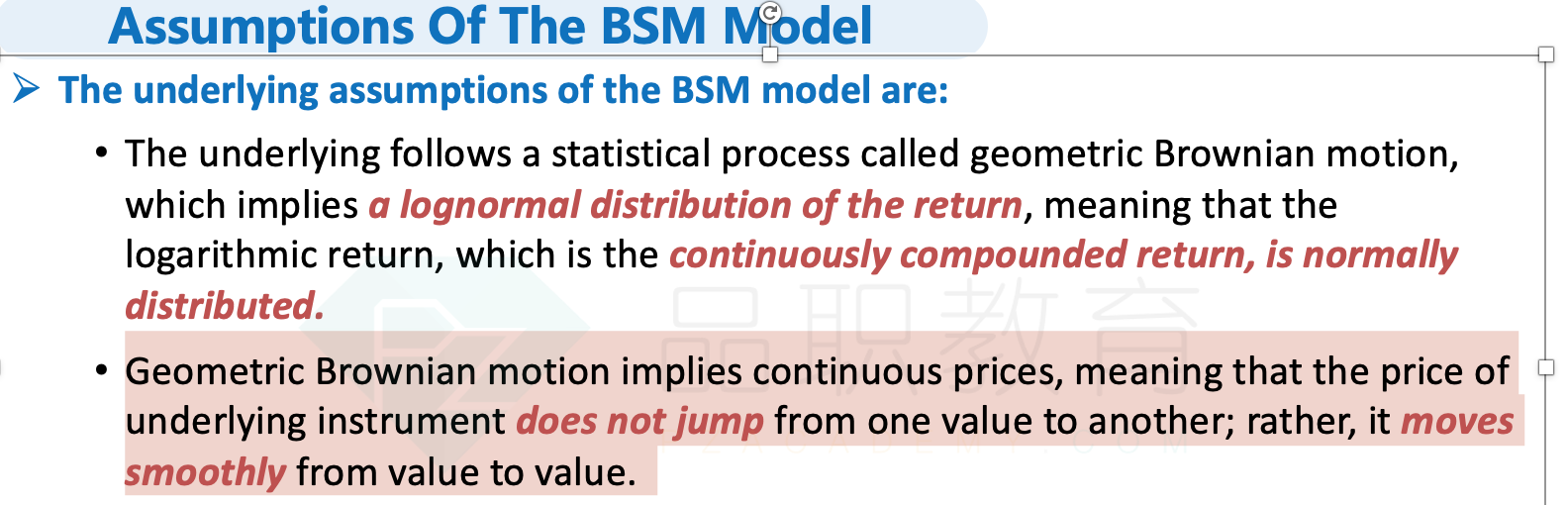

1.Lee’s statement about the assumptions of the BSM model is accurate with regard to:

选项:

A. interest rates but not continuous prices.

B. continuous prices but not the return distribution.

C. the stock return distribution but not the volatility.

解释:

B is correct.

Although the BSM model assumes continuous stock prices, it also assumes that stock returns are lognormally distributed (not normally distributed).

a选项哪里错了,利率恒定,价格不连续啊