NO.PZ201709270100000206

问题如下:

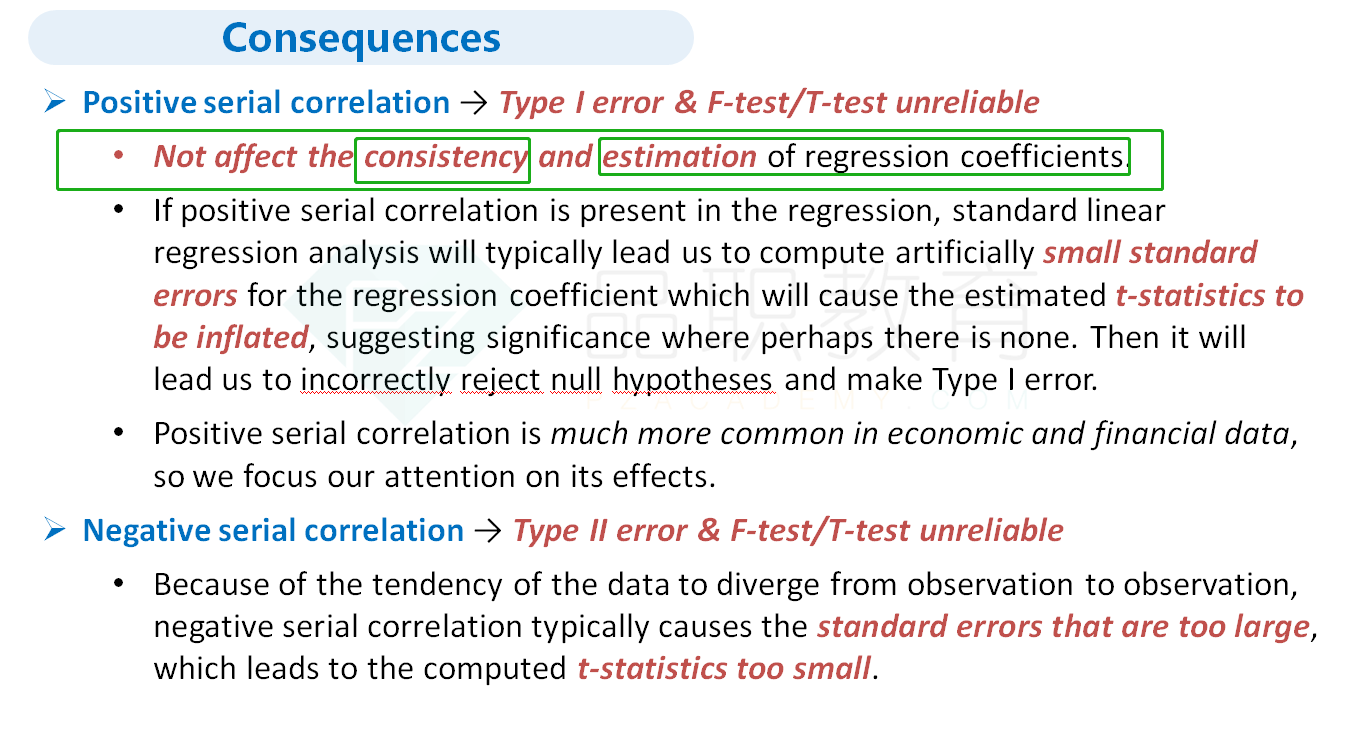

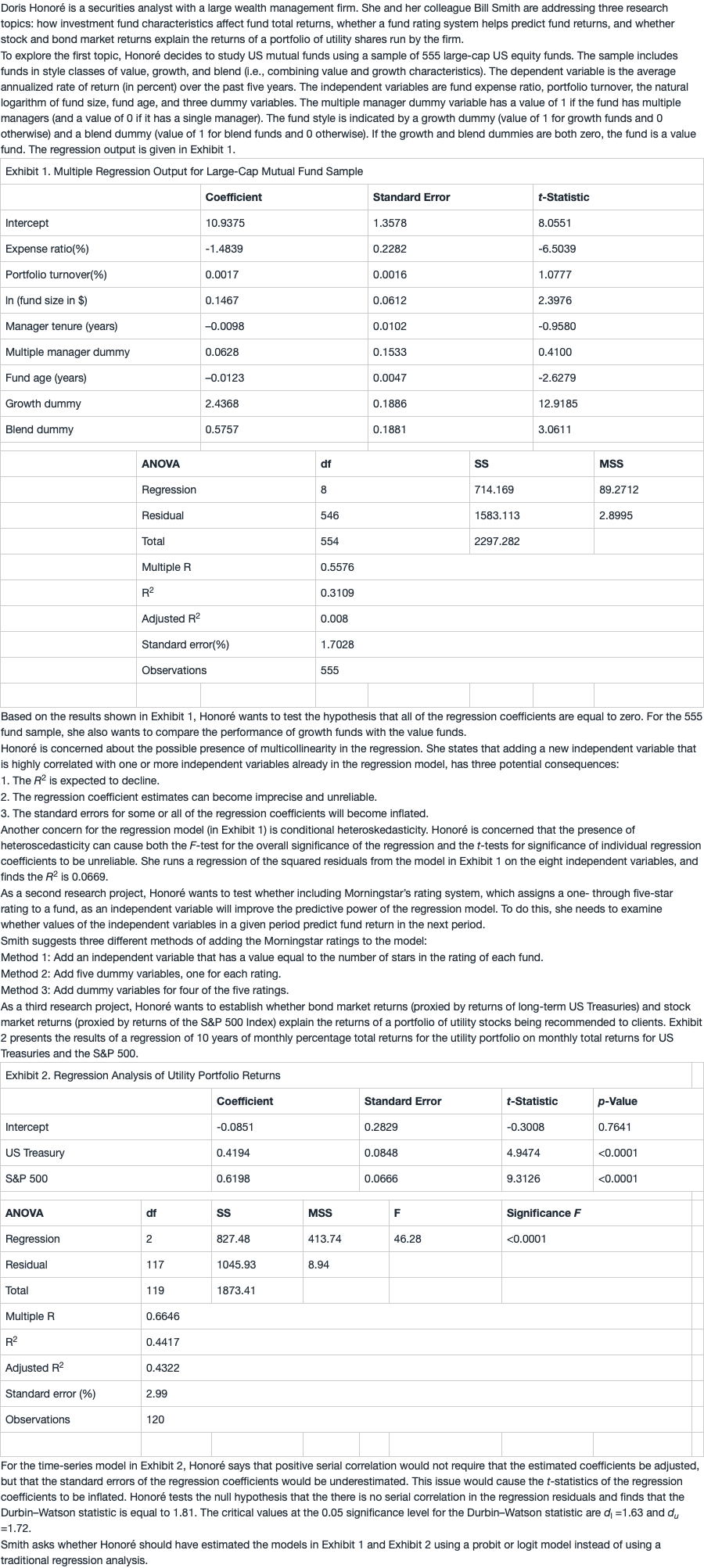

6. Is Honoré’s description of the effects of positive serial correlation (in Exhibit 2) correct regarding the estimated coefficients and the standard errors?

选项: Yes

No, she is incorrect about only the estimated coefficients

C.No, she is incorrect about only the standard errors of the regression coefficients

解释:

A is correct. The model in Exhibit 2 does not have a lagged dependent variable. Positive serial correlation will, for such a model, not affect the consistency of the estimated coefficients. Thus, the coefficients will not need to be corrected for serial correlation. Positive serial correlation will, however, cause the standard errors of the regression coefficients to be understated; thus, the corresponding t-statistics will be inflated.

请问这道题为什么不影响estimates的估计?