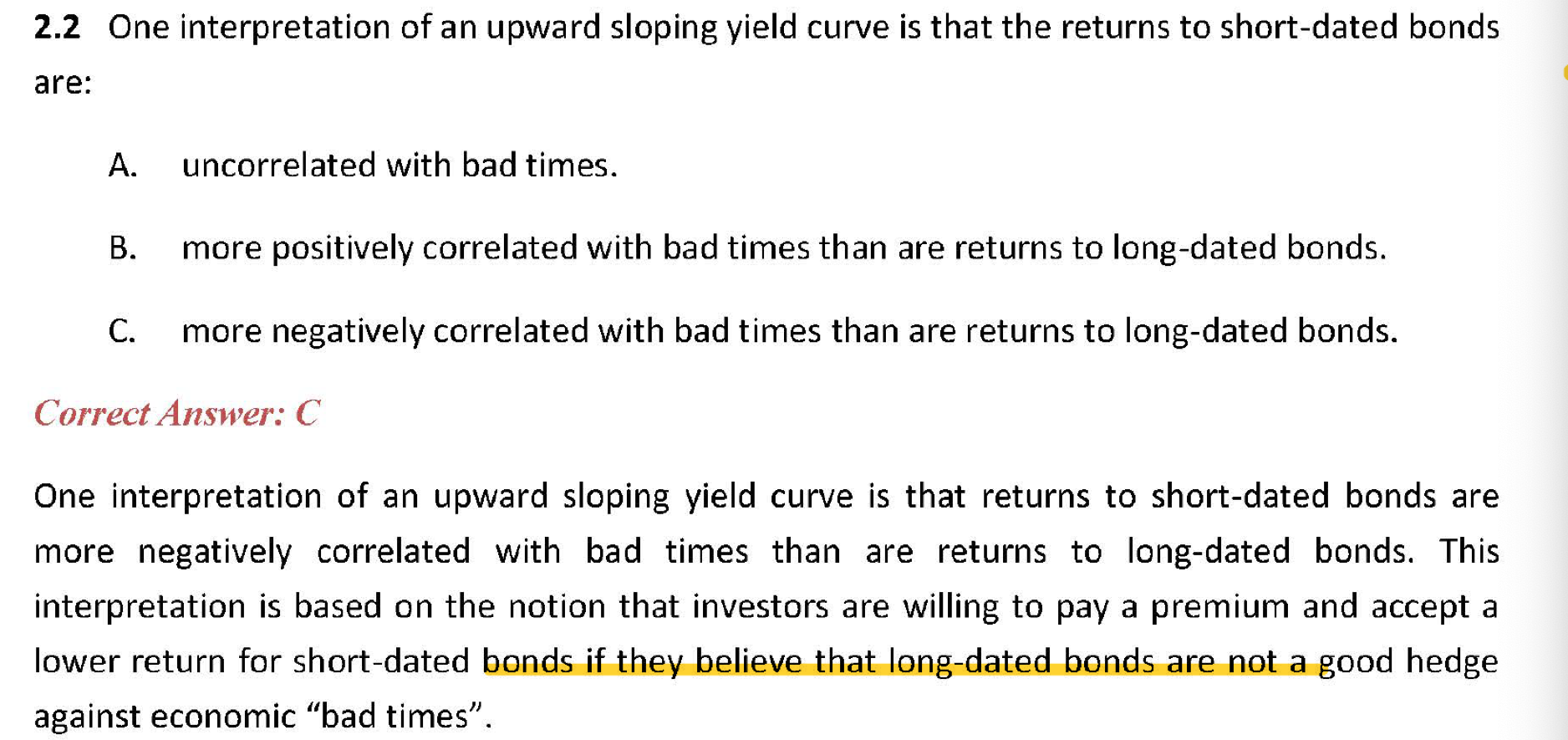

2.2的C选项和1.6答案划黄线的部分,这俩不矛盾吗?real short-term interest rates 和return to short-dated bonds是一个东西吧?

为啥bad times是负相关(自变量上升,因变量下降),然后1.6又说positively related?

星星_品职助教 · 2021年05月18日

同学你好,

real short-term interest rates 和return to short-dated bonds是两个不同的知识点。

从利率角度出发分析,real interest rate是没有通货膨胀的,但short-dated bonds的利率是含有通货膨胀因素在的。

在real interest rate知识点下讲了higher trend real economic growth have higher real default-free interest rates,即经济增长更快的地方利率更高。和The real interest rates are higher in an economy in which GDP growth is more volatile即经济不稳定的地方利率更高。

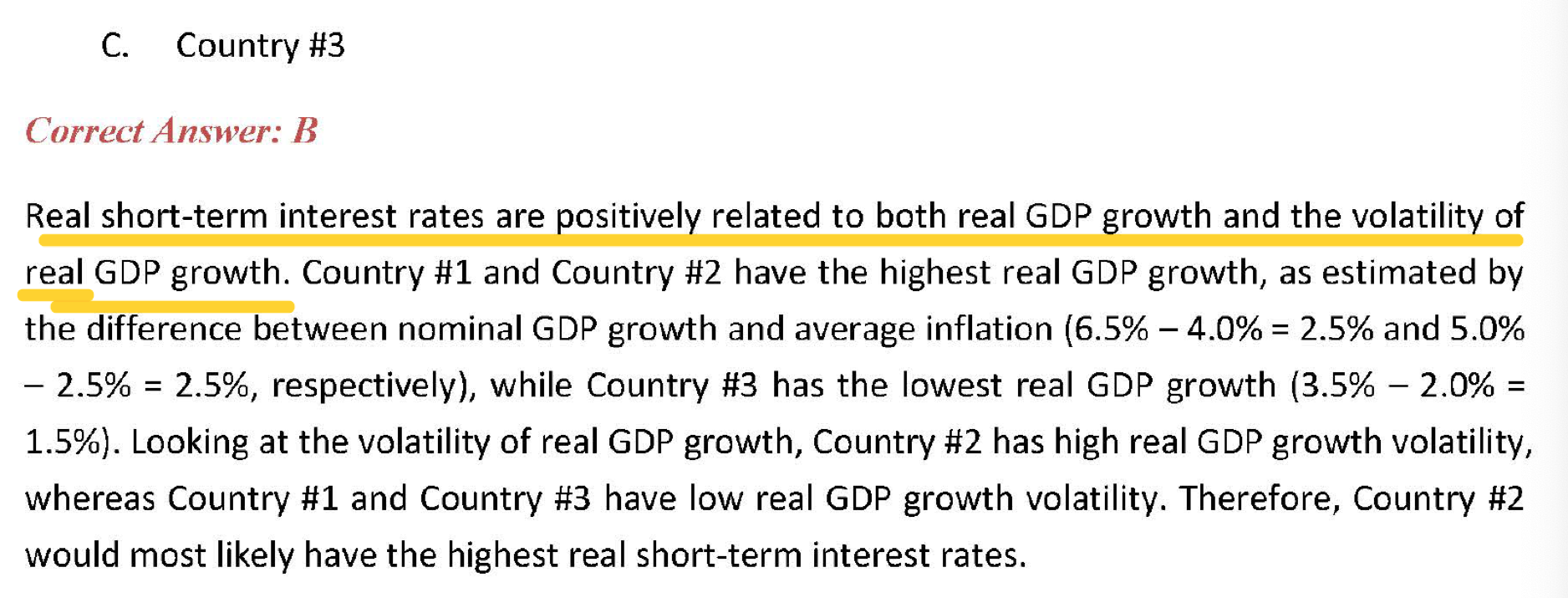

这是1.6题 positive correlated的答案。

-----------------

从考点角度出发分析,2.2题考察的不是利率。

return to short-dated bonds是return的概念。return=coupon+capital gain。

所以2.2题是另外的一个分析角度:

short-dated bonds是避险产品,有对冲经济下滑消费下降的作用。由于是对冲,所以必然和bad times(经济下滑)是negative correlated。