NO.PZ201909300100000301

问题如下:

1 Of the three attribution approaches referenced by Tolmach, the method requested by the committee:

选项:

A.is the least accurate.

uses the underlying holdings of the actual portfolio.

is the most difficult and time consuming to implement.

解释:

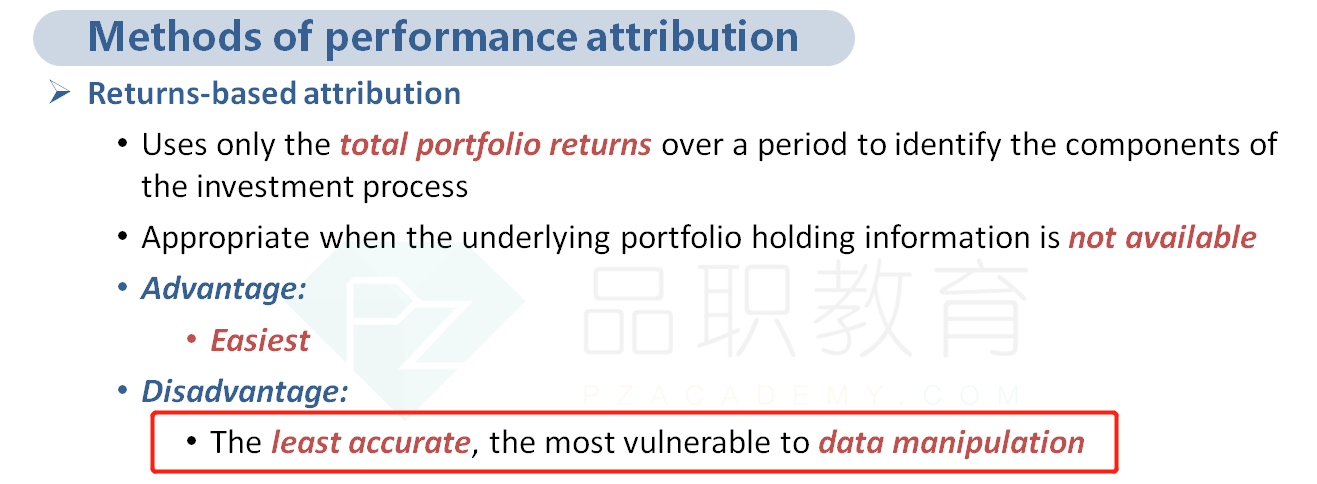

A is correct.

The committee described a return-based attribution, which is the least accurate of the three approaches (the return-based, holdings-based, transaction-based approaches). Return-based attribution uses only the total portfolio returns over a period to identify the components of the investment process that have generated the returns.

没读懂题,请老师解释一下 正文 及题目