NO.PZ2018122701000012

问题如下:

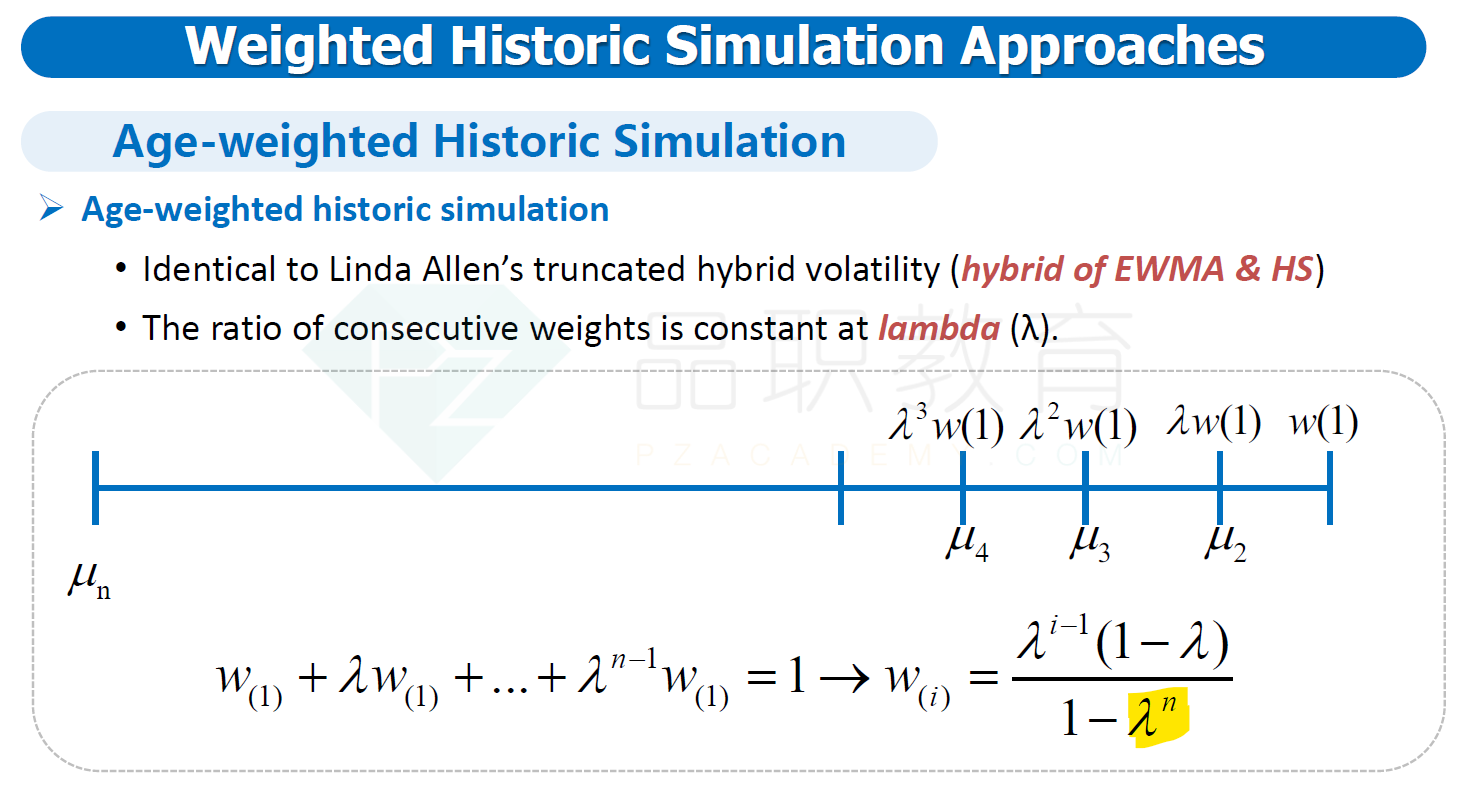

Jack has collected a large data set of daily market returns for three emerging markets and he want to compute the VaR. He is concerned about the non-normal skew in the data and is considering non-parametric estimation methods. Which of the following statements about Age-weighted historical simulation approach is most accurate?

选项:

A. The age-weighted procedure incorporate

estimates from GARCH model.

B. If the decay factor in the model is close to

1, there is persistence within the data set.

C. When using this approach, the weight

assigned on day i is equal to

D. The number of observation should at least

exceed 250.

解释:

B is correct.

考点Age-weighted historical simulation

解析If the intensity parameter (i.e., decay factor) is close to 1, there will be persistence (i.e., slow decay) in the estimate. The expression for the weight on day ihasiin the exponent when it should be n. While a large sample size is generally preferred, some of the data may no longer be representative in a large sample.

选项c为什么错呢呀??