NO.PZ201512020300000803

问题如下:

Elena Vasileva recently joined EnergyInvest as a junior portfolio analyst. Vasileva’s supervisor asks her to evaluate a potential investment opportunity in Amtex, a multinational oil and gas corporation based in the US. Vasileva’s supervisor suggests using regression analysis to examine the relation between Amtex shares and returns on crude oil.

Vasileva notes the following assumptions of regression analysis:

Assumption 1 The error term is uncorrelated across observations.

Assumption 2 The variance of the error term is the same for all observations.

Assumption 3 The expected value of the error term is equal to the mean value of the dependent variable.

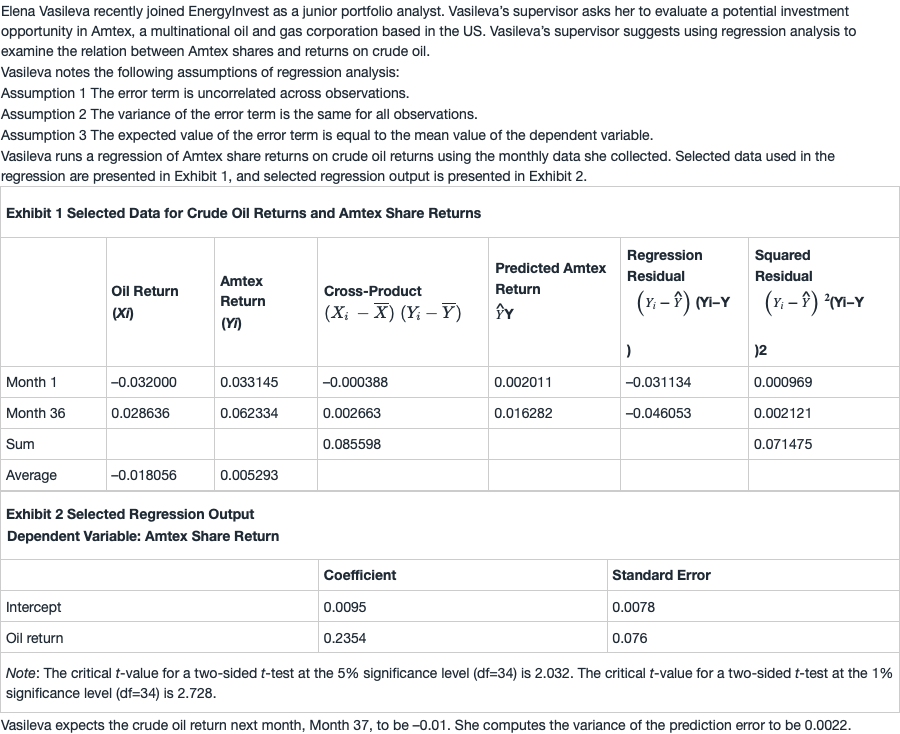

Vasileva runs a regression of Amtex share returns on crude oil returns using the monthly data she collected. Selected data used in the regression are presented in Exhibit 1, and selected regression output is presented in Exhibit 2.

Vasileva expects the crude oil return next month, Month 37, to be –0.01. She computes the variance of the prediction error to be 0.0022.

Based on Exhibit 2, Vasileva should reject the null hypothesis that:

选项:

A.the slope is less than or equal to 0.15

the intercept is less than or equal to 0

crude oil returns do not explain Amtex share returns.

解释:

C is correct. Crude oil returns explain the Amtex share returns if the slope coefficient is statistically different from zero. The slope coefficient is 0.2354 and is statistically different from zero because the absolute value of the t-statistic of 3.0974 is higher than the critical t-value of 2.032 (two-sided test for n – 2 = 34 degrees of freedom and a 5% significance level):

t-statistic =( 0.2354-0.0000)/

0.0760=3.0974

Therefore, Vasileva should reject the null hypothesis that crude oil returns do not explain Amtex share returns because the slope coefficient is statistically different from zero.

请问A和B是如何得到拒绝这两个假设的,也同样是计算t值,然后看是否落在置信区间吗?谢谢