NO.PZ2019103001000026

问题如下:

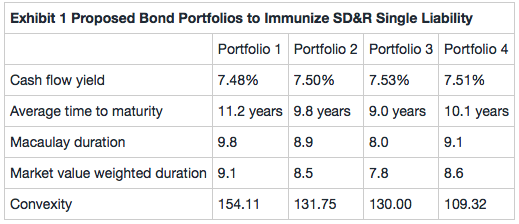

Mowery informs Compton that DFC has a single $500 million liability due in nine years, and she wants SD&R to construct a bond portfolio that earns a rate of return sufficient to pay off the obligation.

Compton provides the four US dollar–denominated bond portfolios in Exhibit 1 for consideration. Compton explains that the portfolios consist of non-callable, investment-grade corporate and government bonds of various maturities because zero-coupon bonds are unavailable.

Based on Exhibit 1, which of the portfolios will best immunize SD&R’s single liability?

选项:

A.

Portfolio 1

B.

Portfolio 2

C.

Portfolio 3

解释:

B is correct.

In the case of a single liability, immunization is achieved by matching the bond portfolio’s Macaulay duration with the horizon date. DFC has a single liability of $500 million due in nine years. Portfolio 2 has a Macaulay duration of 8.9, which is closer to 9 than that of either Portfolio 1 or 3. Therefore, Portfolio 2 will best immunize the portfolio against the liability.