- The level of active risk will rise with an increase in idiosyncratic volatility.

- The active risk attributed to Active Share will be smaller in more diversified portfolios.

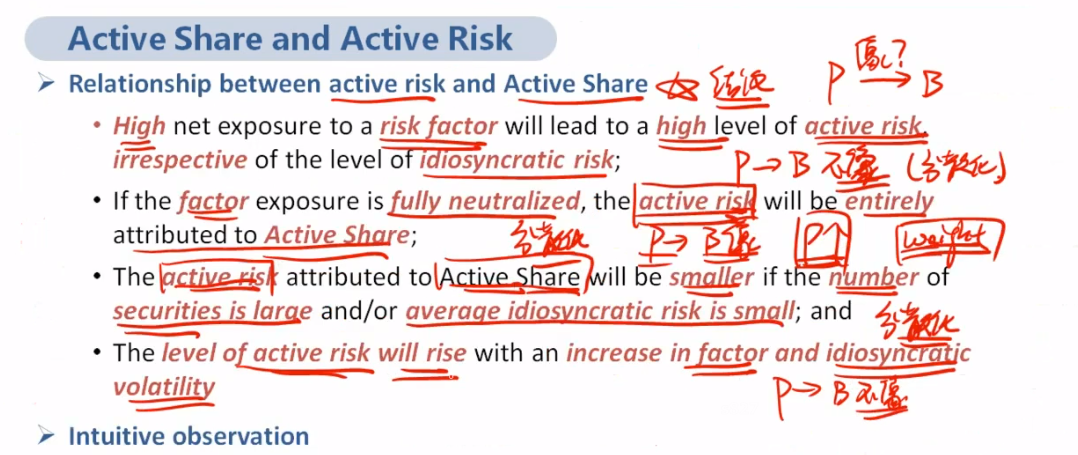

- If the factor exposure is fully neutralized, the Active Share will be entirely attributed to the active risk.

这三句话判断对错,我有点晕了,老师可以帮每句解释一下吗?第一句idiosyncratic volatility是什么意思呀?

The comment concerning neutralizing factor exposure is incorrect: In a single-factor model, if the factor exposure is neutralized, the active risk will be entirely attributable to the Active Share—a consequence of the manager deviating from benchmark weights. The active risk attributed to Active Share will be smaller for more diversified portfolios with lower idiosyncratic risk. Active risk does rise with an increase in factor and idiosyncratic volatility.