NO.PZ2016082406000004

问题如下:

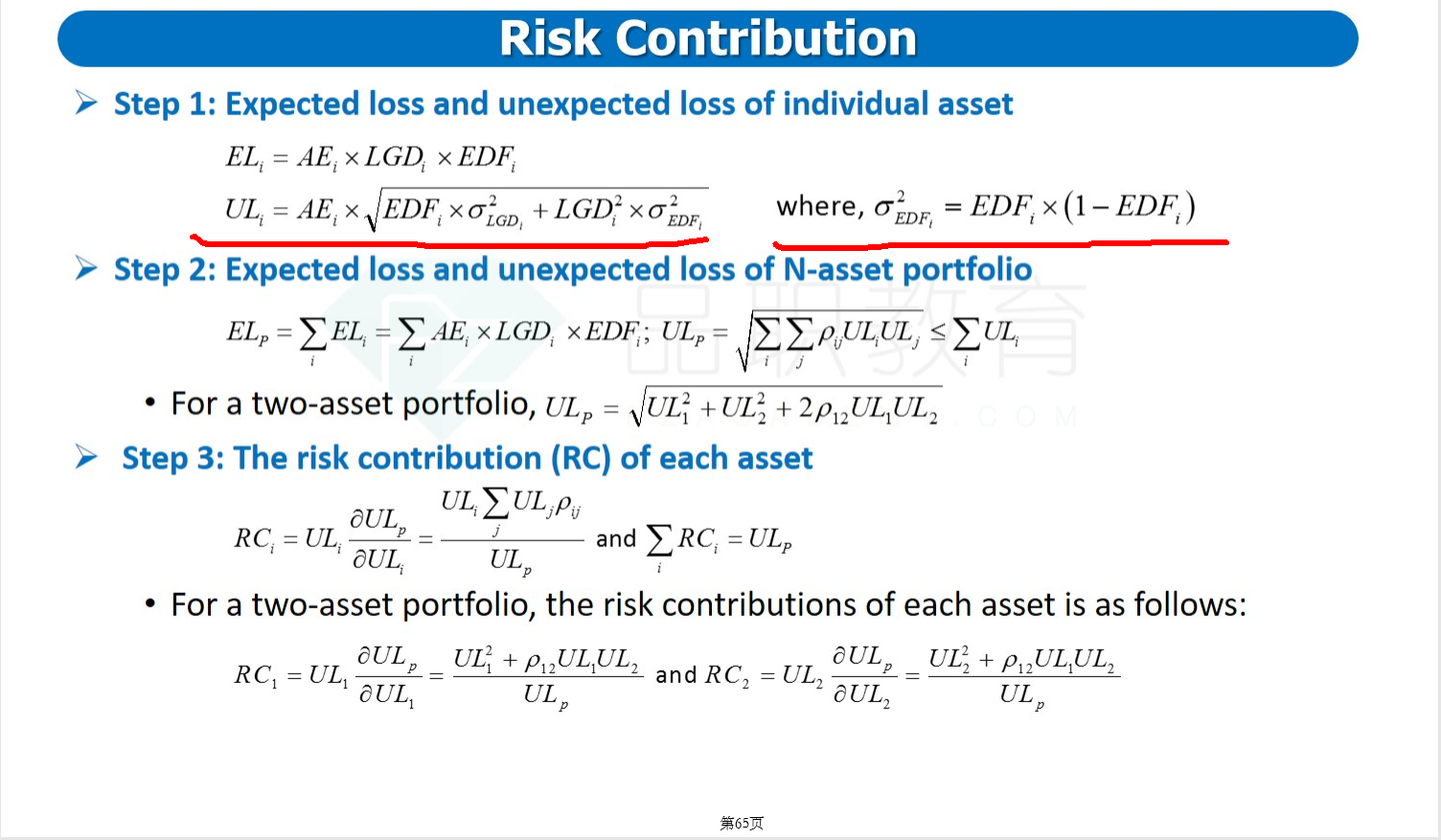

A bank has booked a loan with total commitment of $50,000 of which 80% is currently outstanding. The default probability of the loan is assumed to be 2% for the next year and loss given default (LGD) is estimated at 50%. The standard deviation of LGD is 40%. Drawdown on default (i.e., the fraction of the undrawn loan) is assumed to be 60%. The expected and unexpected losses (standard deviation) for the bank are

选项: Expected

loss = $500, unexpected loss = $4,140

Expected loss = $500, unexpected loss = $3,220

C.Expected loss = $460, unexpected loss = $3,220

D.Expected loss = $460, unexpected loss = $4,140

解释:

ANSWER: D

First, we compute the exposure at default. This is the drawn amount, or 80%x$50,000=$40,000 plus the drawdown on default, which is 60%x$10,000=$6,000, for a total of CE= $46,000. The expected loss is this amount times ₤or EL = $460. Next, we compute the standard deviation of losses using Equation: . The variance is . Taking the square root gives 0.090. Multiplying by $46,000 gives $4,140. Ignoring gives the incorrect answer of $3,220. Note that the unexpected loss is much greater than the expected loss.

为什么公式里是standard deviation of PD,没有^2?