NO.PZ2018111303000025

问题如下:

Fabian, CFA, work on the Equity investment company. Golden Elementary school paid ¥360 million to purchase 50 percent Frost Early Education Center on 31 December 2018. The excess of the purchase price over the fair value of Frost’s net assets was attributable to previously unrecorded licenses. These licenses were estimated to have an economic life of five years. The fair value of Frost’s assets and liabilities other than licenses was equal to their recorded book value.

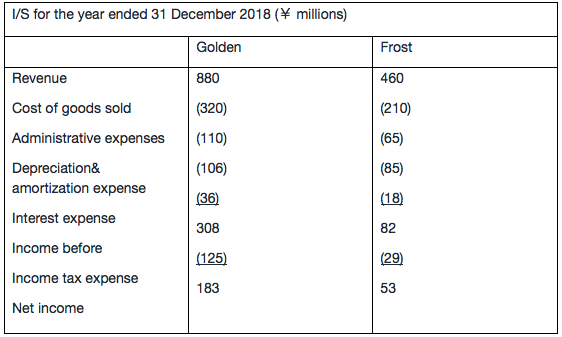

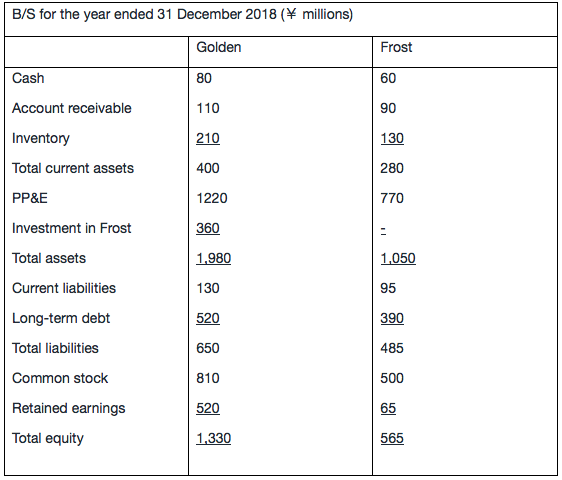

Golden and Frost’s condensed income statements for the year ended 31 December 2018, and Balance Sheet are presented the following table:

Golden’s current ratio on 31 December 2018 most likely will be highest if the results of the acquisition are reported using:

选项:

A.the equity method

B.consolidation with full goodwill

C.consolidation with partial goodwill

解释:

A is correct.

考点:不同合并会计报表方法下,会计比率的对比。

解析:

equity method是一项合并,不合并子公司的资产和负债,current ratio =400/130=3.08

consolidation需要合并子公司的全部资产和负债,current ratio= (400+280)/(130+95)=3.02

3.08大于3.02,所以选A。

partial goodwill与full goodwill的方式不影响current asset的金额,影响的是goodwill的金额,而goodwill属于长期资产。

老师,之前有道类似的题目,在三个方法里选,而equity method因为投资比例超过50%而被排除,这道题里为啥不因为这个理由排除?