问题如下图:

选项:

A.

B.

C.

D.

用10天的var 才对吧

解释:

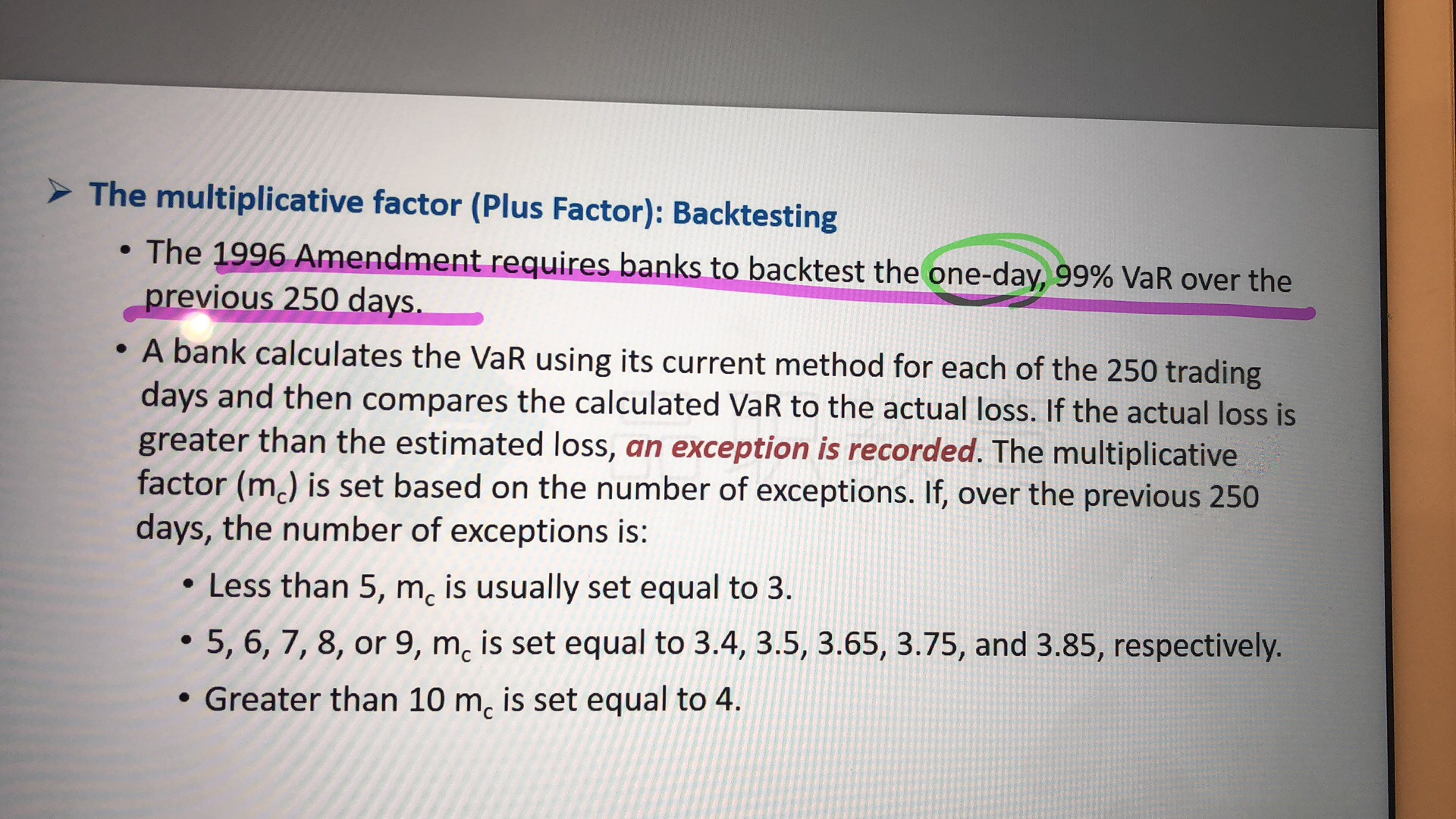

NO.PZ2016070202000005 问题如下 Backtesting routinely compares ily profits anlosses with mol-generaterisk measures to gauge the quality anaccuraof their risk measurement systems. The 1996 Market Risk Amenent scribes the backtesting framework this to accompany the internmols capitrequirement. This backtesting framework involvesI. The size of outliersII. The use of risk measure calibrateto a one-y holng perioII. The size of outliers for a risk measure calibrateto a 10-y holng perioV. Number of outliers A.II anIII B.II only C.I anII II anIV is correct. The backtesting framework in the IMA only counts the number of times a ily exception occurs (i.e., a loss worse thVAR). So, this involves the number of outliers anthe ily Vmeasure. 如题

NO.PZ2016070202000005 老师可否2、3的差异,3错在哪里了

NO.PZ2016070202000005 II only I anII II anIV is correct. The backtesting framework in the IMA only counts the number of times a ily exception occurs (i.e., a loss worse thVAR). So, this involves the number of outliers anthe ily Vmeasure.老师好,巴塞尔协议对信用风险、市场风险、操作风险置信区间、时间间隔…是怎么规定的?还有为什么这么规定?我一直没有记住和搞混?非常感谢!

NO.PZ2016070202000005 请问这道题在课件的哪个地方有体现?

NO.PZ2016070202000005 1. calibrateto a one-y holng perio2. calibrateto a ten-y holng perio我知道10天的VAR是通过ily VAR去推出来的,所以这两种说法感觉第二种更对吧?就是(通过ily)调整成10天期限的VAR。而不是说直接调整成1天期限的VAR。