NO.PZ2016082405000108

问题如下:

Teresa Harrison, a junior portfolio manager, is considering the purchase of super senior tranches for her client portfolios. The epical client is fairly conservative and concerned more with downside risk than upside potential. Harrison based her recommendation on the following observations:

•Senior tranches have large attachment points and hence a low probability of credit losses.

•Mezzanine tranches represent the first loss piece of the capital structure.

•Synthetic CDOs have standardized tranche widths similar to index tranches.

How many of these observations support Harrison's view of tranches?

选项:

A.0.

B.1.

C.2.

D.3.

解释:

B Only recommendation 1 is correct. Senior tranches have a low probability of default because their attachment points are much higher in the capital structure. Equity tranches represent the first loss position. Index tranches, not synthetic CDOs, have standardized tranche widths.

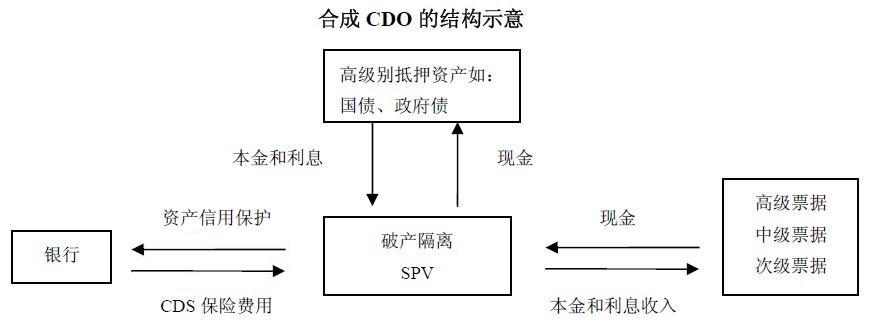

Synthetic CDOs 就是普通的CDO吧?