NO.PZ201602060100001006

问题如下:

6. Based on Byron’s forecast, NinMount’s 2019 total asset turnover ratio on beginning assets under the equity method is most likely:

选项:

A.lower than if the results are reported using consolidation.

B.the same as if the results are reported using consolidation.

C.higher than if the results are reported using consolidation.

解释:

A is correct.

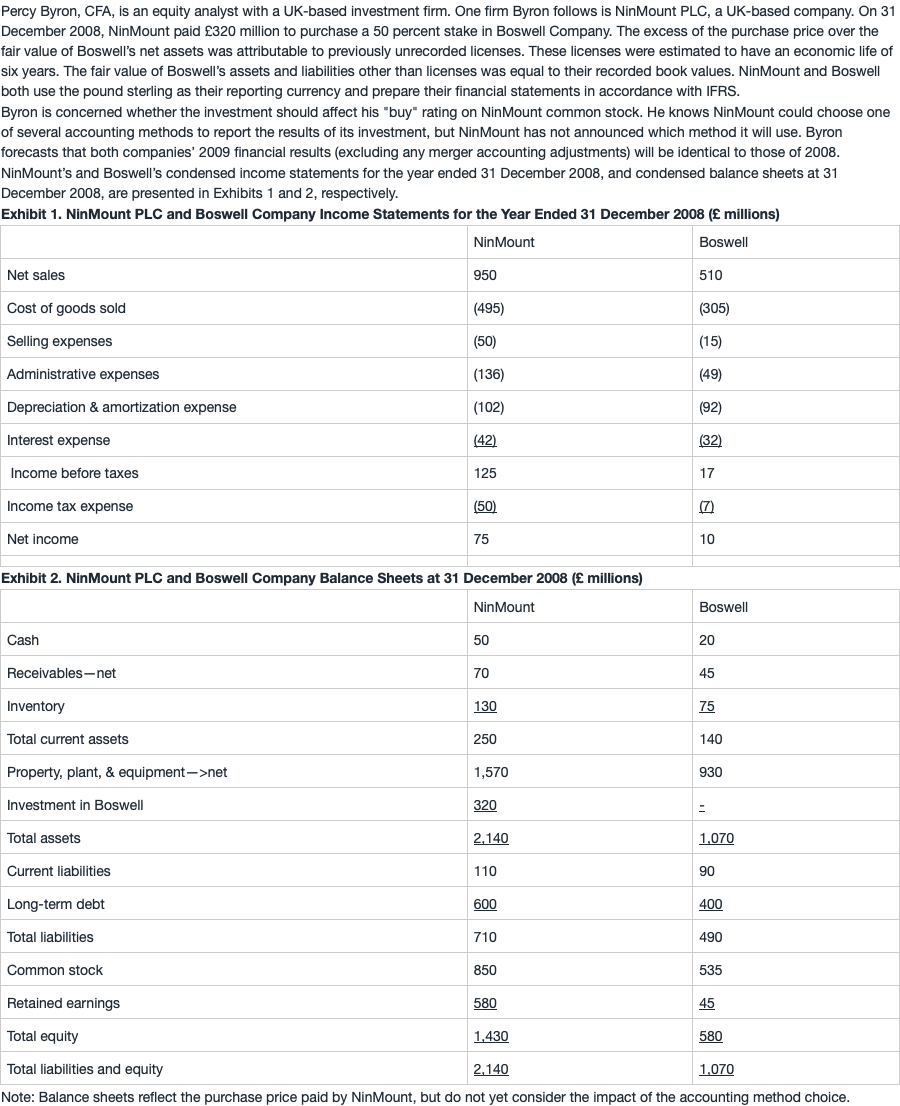

Using the equity method, Total asset turnover = Net sales/Beginning total assets = £950/£2,140 = 0.444. Total asset turnover on beginning assets using consolidation = £1,460/£2,950 = 0.495. Under consolidation, Assets = £2,140 -320 + 1,070 + 60 = £2,950. Therefore, total asset turnover is lowest using the equity method.

考点 : 不同的合并会计报表方法对 会计比率的影响。

解析 :

Total asset turnover = Net sales/Beginning total assets

对于equity method来说,Total asset turnover = Net sales/Beginning total assets = £950/£2,140 = 0.444

对于consolidation method来说,Assets = £2,140 -320 + 1,070 + 60 = £2,950,且需合并收入,Total asset turnover = £1,460/£2,950 = 0.495

在equity method下,total asset turnover 更低。

对于consolidation method下asset的计算特别说明一下:

-320是因为在合并里需要扣除母公司个报中的investment这一项,因为consolidation需要全额合并子公司的资产和负债,这就相当于合并了子公司的权益。而investment即是对子公司权益的投资,如果在合并时不扣除investment这一项,就会重复记账。

+60是因为子公司有一项未记账的资产,在合并时需要加回。

老师,这道题目可以再详细解答一下吗?我不太明白consolidation的处理