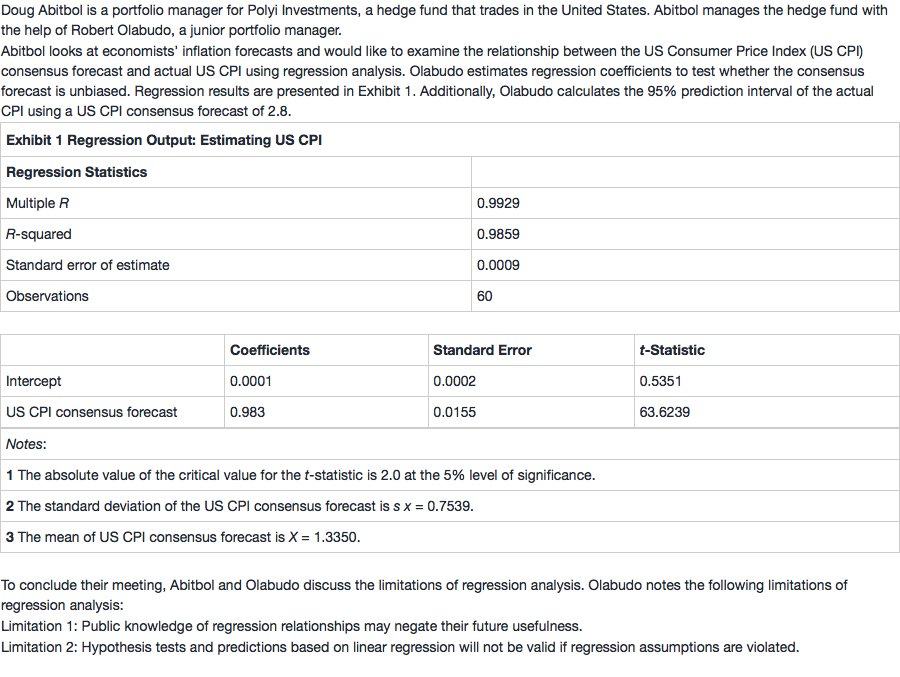

NO.PZ201512020300000902

问题如下:

Based on Exhibit 1, Olabudo should calculate a prediction interval for the actual US CPI closest to:

选项:

A.2.7506 to 2.7544

B.2.7521 to 2.7529

C.2.7981 to 2.8019.

解释:

A is correct. The prediction interval for inflation is calculated in three steps:

Step 1 – Make the prediction given the US CPI forecast of 2.8:

Y=b0+b1X=0.0001+(0.9830×2.8)=2.7525

Step 2 – Compute the variance of the prediction error:

sf2=s2[1+n1+(n−1)×sx2(X−X)2]

sf2=0.00092[1+601+(60−1)×0.75392(2.8−1.3350)2]=0.00000088

sf=0.0009

Step 3 – Compute the prediction interval:

Y±tc×sf

2.7525±(2.0×0.0009)

2.7525–(2.0×0.0009)=2.7506; lower bound

2.7525+(2.0×0.0009)=2.7544; upper bound

So, given the US CPI forecast of 2.8, the 95% prediction interval is 2.7506 to 2.7544.

为什么不可以用文中表格给出的standard error