NO.PZ201512020300000901

问题如下:

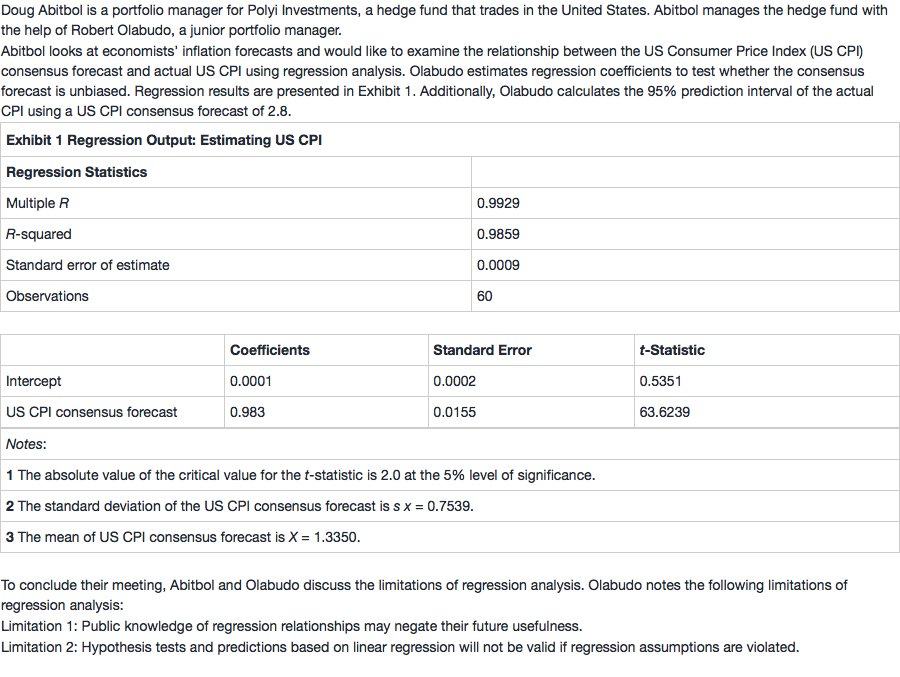

Based on Exhibit 1, Olabudo should:

选项:

A.conclude that the inflation predictions are unbiased.

reject the null hypothesis that the slope coefficient equals 1.

reject the null hypothesis that the intercept coefficient equals 0.

解释:

A is correct. If the consensus inflation forecast is unbiased, then the intercept, b0, should equal 0, and the slope coefficient, b1, should equal 1. The t-statistic for the intercept coefficient is 0.5351, which is less than the critical t-value of 2.0, so the intercept coefficient is not statistically different than 0. To test whether the slope coefficient equals 1, the t-statistic is calculated as: t=–1.0968

Because the absolute value of the t-statistic of –1.0968 is less than the critical t-value of 2.0, the slope coefficient is not statistically different than 1. Therefore, Olabudo can conclude that the inflation forecasts are unbiased.

If the consensus inflation forecast is unbiased, then the intercept, b0, should equal 0, and the slope coefficient, b1, should equal 1. 怎么理解。为啥无偏有这个要求?