发亮_品职助教 · 2021年04月17日

嗨,爱思考的PZer你好:

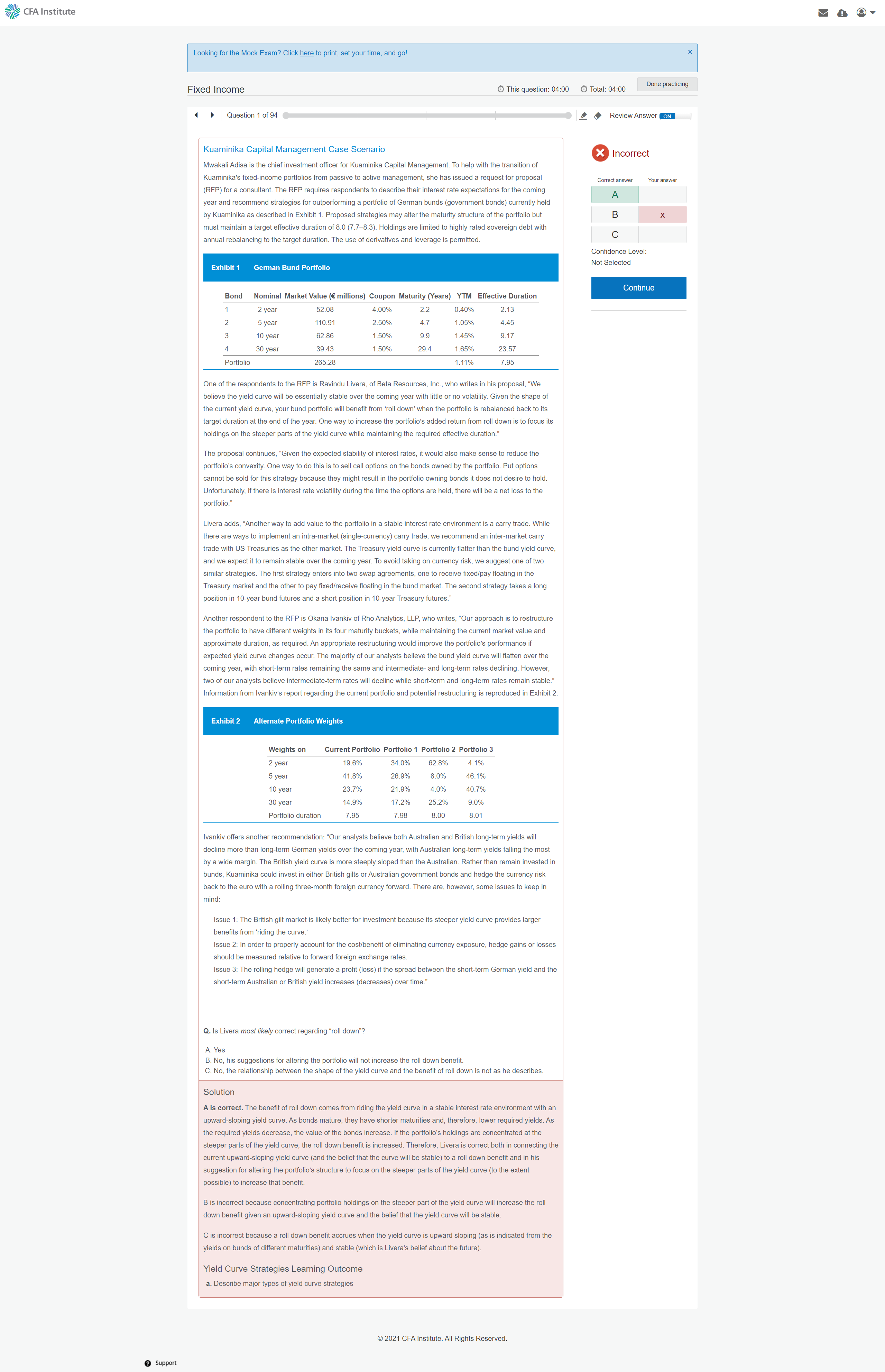

这道题其实考察的就是Rolldown return的基础原理。

那Rolldown return的核心就是:

(1)预期收益率曲线Stable,且收益率曲线向上倾斜,即,长期利率大于短期利率。

(2)投资期初,债券是一个较长期的债券,债券的折现率较高,投资期末,债券变成了较短期的债券,由于长期利率大于短期利率,那投资期末债券的折现率会变得更低。那这样的话,期末的折现率更低,债券会有价格上升,于是,投资期末与期初之间会存在着买卖价差,这个买卖价差就是Rolldown renturn的收益。

(3)收益率曲线越陡峭,Rolldown return的收益就越大。收益率曲线越陡峭,就代表期末债券的折现率会远远地小于期初债券的折现率,那这样的话,期末债券折现率会大幅下降,即,期末债券的价格会大幅上升,这个Rolldown return的收益就会很大。所以,收益率曲线越陡峭,Rolldown return赚取的收益就越大。

具体Rolldown return前几天有一个详细的解释,可以参考:

https://class.pzacademy.com/qa/73848

明白了以上原理,现在就针对答案做一下回复:

下面这句说,在利率预期稳定(Stable),Upward-sloping时,Riding the yield curve可以带来Roll down return的收益,这点正确。就是最基础的原理。

The benefit of roll down comes from riding the yield curve in a stable interest rate environment with an upward-sloping yield curve.

这句说,随着我们投资债券,债券的期限变短,那他的折现率就会更低,因此债券在投资期末的价格会上升,这点正确,投资期末债券价格的上升就是rolldown return的收益来源:

As bonds mature, they have shorter maturities and, therefore, lower required yields. As the required yields decrease, the value of the bonds increase.

这句说,如果我们在收益率曲线上最陡峭的部位做Rolldown return,那么Rolldown return的收益还会进一步上升。这点也完全正确,因为越陡峭,代表期初折现率与期末折现率的差异就越大,即,期末为债券折现的折现率会大幅下降,那就会使得债券期末的价格大幅上升,于是使得Rolldown return的收益大幅上升。

If the portfolio’s holdings are concentrated at the steeper parts of the yield curve, the roll down benefit is increased.

基于以上的分析,题干里这个Livera的建议:在Upward-sloping,stable时,做Rolldown return有收益,并且在收益率曲线更陡峭的一段做Rolldown return的收益会更大,下面这句就是这个意思。

Therefore, Livera is correct both in connecting the current upward-sloping yield curve (and the belief that the curve will be stable) to a roll down benefit and in his suggestion for altering the portfolio’s structure to focus on the steeper parts of the yield curve (to the extent possible) to increase that benefit.

----------------------------------------------

加油吧,让我们一起遇见更好的自己!