NO.PZ2016082406000048

问题如下:

Assume that a bank enters into a USD 100 million, four-year annual-pay interest rate swap, where the bank receives 6% fixed against 12-month LIBOR. Which of the following numbers best approximates the current exposure at the end of year 1 if the swap rate declines 125 basis points over the year?

选项:

A.USD 3,420,069

B.USD 4,458,300

C.USD 3,341,265

D.USD 4,331,382

解释:

ANSWER: A

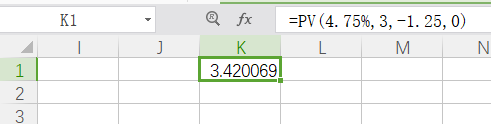

The value of the fixed-rate bond is . Subtracting $100 for the floating leg gives an exposure of $3.4 million. More intuitively, the sum of the coupon difference is 3 times , or around $3.75 million without discounting.

More intuitively, the sum of the coupon difference is 3 times {(6%-4.75%)}\$100=$1.25

(6%−4.75%)$100=$1.25, or around $3.75 million without discounting.