问题如下图:

选项:

A.

B.

C.

解释:

expected market return=Rf+MRP(market risk premium),这是为什么呢?是因为βm=1吗?

李宗_品职助教 · 2018年01月04日

Hi ciaoyy,expected market return=Rf+beta*MRP,这里Beta题目中已经给出了,并不等于1. 解释中已经给出了方程解答过程,请参考,谢谢!

ciaoyy · 2018年01月04日

请问根据CAPM模型,expected return for tghe market指的是beta*MRP?为什么不是MRP呢?这样想的原因是因为beta是针对个股而言的。

ciaoyy · 2018年01月04日

您好,题目问的是expected return for the market,参考答案解析第3行‘the expected rate of return for the market is 9%’。所以可以判断这道题用的是βm=1,因为3+1*(8.4/1.4)=9。是这样吧?

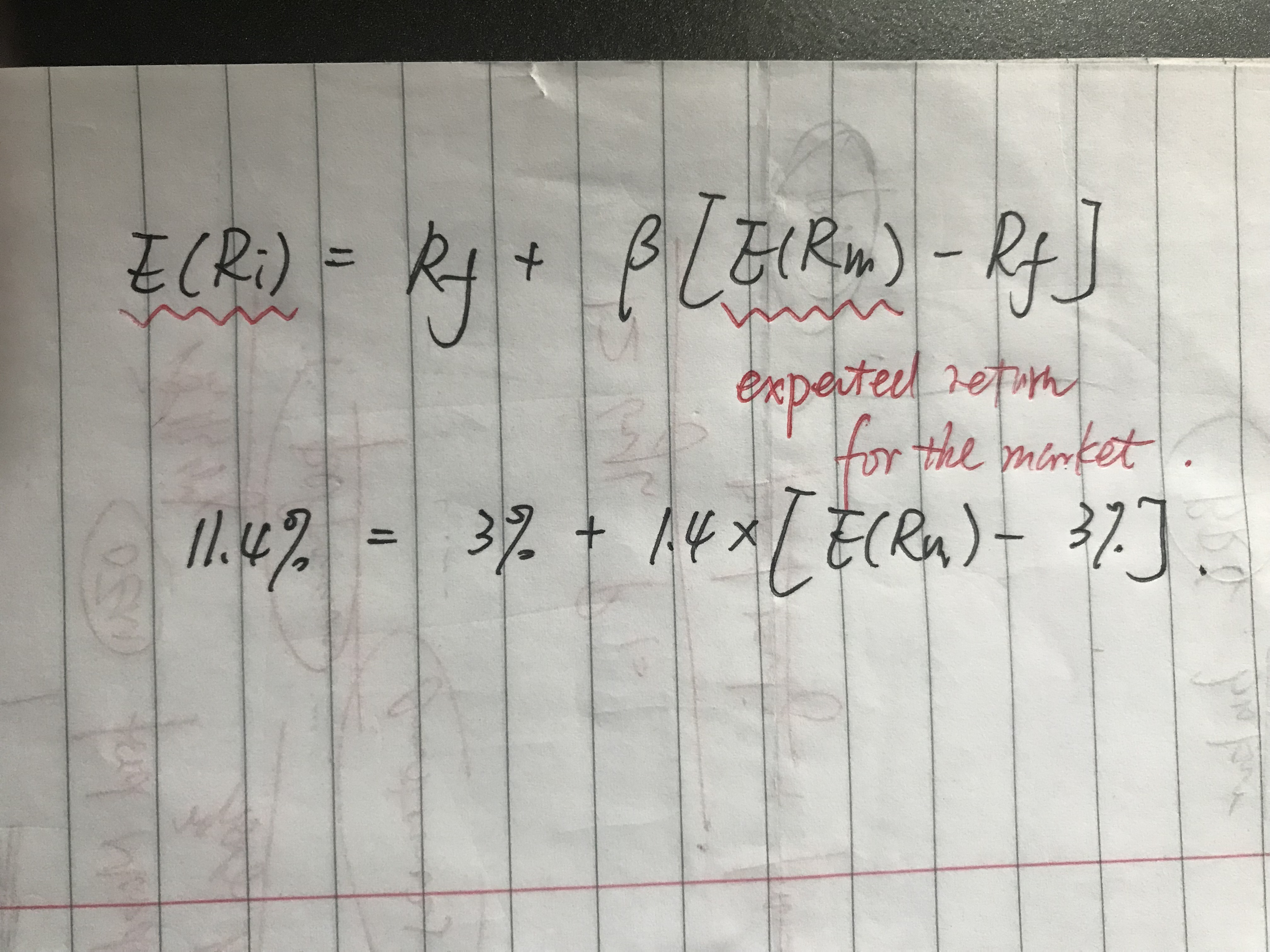

NO.PZ2015121801000103 问题如下 analyst gathers the following information: With respeto the capitasset pricing mol, if expectereturn for Security 2 is equto 11.4% anthe risk-free rate is 3%, the expectereturn for the market is closest to: A.8.4%. B.9.0%. C.10.3%. is correct.The expecterisk premium for Security 2 is 8.4%, (11.4% − 3%), incates ththe expectemarket risk premium is 6%; therefore, sinthe risk-free rate is 3% the expecterate of return for the market is 9%. This, using the CAPM, E(Ri) = Rf +βi[E(Rm)–Rf], 11.4% = 3% + 1.4(X%), where X% = (11.4% − 3%)/1.4 = 6.0% = market risk premium. 题目让求的是expereturn for market,答案给的是market risk premium,是不是错了

老师,这题答案要求的shi2expectereturn,为什么答案是risk premium?谢谢