NO.PZ201512020300000502

问题如下:

Assuming regularization is utilized in the machine learning technique used for executing Step 1, which of the following ML models would be least appropriate:

选项:

A.Regression tree with pruning.

LASSO with lambda (λ) equal to 0.

LASSO with lambda (λ) between 0.5 and 1.

解释:

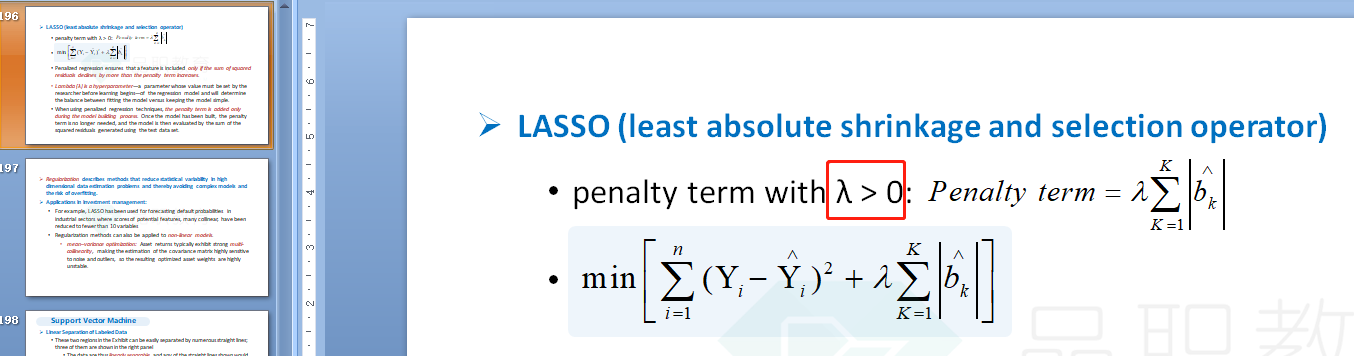

B is correct. It is least appropriate because with LASSO, when λ = 0 the penalty (i.e., regularization) term reduces to zero, so there is no regularization and the regression is equivalent to an ordinary least squares (OLS) regression.

A is incorrect. With Classification and Regression Trees (CART), one way that regularization can be implemented is via pruning which will reduce the size of the regression tree—sections that provide little explanatory power are pruned (i.e., removed).

C is incorrect. With LASSO, when λ is between 0.5 and 1 the relatively large penalty (i.e., regularization) term requires that a feature makes a sufficient contribution to model fit to offset the penalty from including it in the model.

这道题不是很理解,不应该是等于0才能够让惩罚项更有意义吗