NO.PZ2015121810000020

问题如下:

You have a portfolio 100% allocated to a manager with an ex-post active risk at 8.0%. You choose to allocate a 75% position to the active manager and 25% to the benchmark to bring the portfolio back to your target active risk of 6.0%. If the manager’s information ratio is 0.50, what happens to the information ratio of the portfolio after the reallocation?

选项:

A.The information ratio increases because the lower active risk reduces the denominator of the ratio.

B.The information ratio remains unchanged because allocations between the active portfolio and the benchmark don’t affect the information ratio.

C.The information ratio decreases because allocating some of the portfolio to the benchmark means that the external manager generates less active return.

解释:

B is correct.

The information ratio is unaffected by rebalancing the active portfolio and the benchmark portfolio. In this case, the active return and active risk are both reduced by 25%, and the information ratio will be unchanged.

考点:information ratio

解析:结论,information ratio不受aggressiveness的影响。

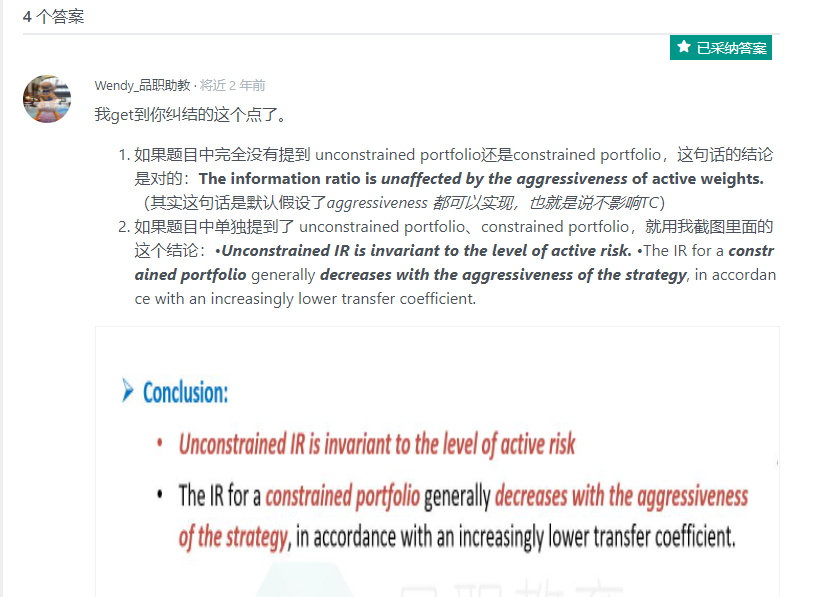

本题,另外一个同学问了之后,老师给出的答案是

“无论是 是unconstrained fund还是constrained fund ,结论都是:

The information ratio is unaffected by the aggressiveness of active weights.”

看完这个解答有点confuse,如下图

那讲义里这句话又怎么理解呢?

随着agressiveness上升,IR随着TC下降而下降吗?