NO.PZ2018062006000126

问题如下:

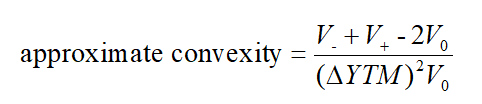

A bond is priced at 88.692 per 100 of par value. The bond's full price will fall to 88.642 if the yield-to-maturity rises by 10 basis points. Moreover, the bond's full price will increase to 88.762 if the yield-to-maturity decreases by 10 basis points. The approximate convexity of the bond is:

选项:

A.105.24.

B.225.50.

C.687.41.

解释:

B is correct.

Approximate convexity

=[88.762+88.642-(2*88.692)]/[(0.001)^2*88.692]

=225.499

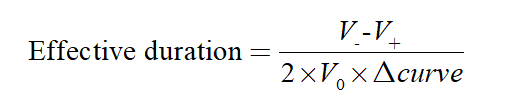

为什么这题的▲y不是 0.001x2 的平方?

我记得之前在算Effective duration的时候, 我们是用的分母算的是有 2吧