问题如下:

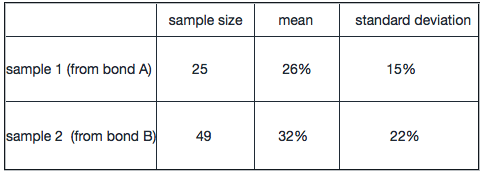

Here is a table discribing sample statistics from two bonds' rate of return which are both normally distributed over the past decades. If an investor is considering whether the mean of bond A is equal to 22%,

which of the following conclusion is least appropriate (significant level=1%) ?

选项:

A. The null hypothesis can be rejected.

B. It is appropriate to use a two-tailed t-test.

C. The test statistic value is 1.333.

解释:

A is correct.

The null hypothesis:

Because the sample size is 25, which is less than 30, so it is appropriate to use the two-tailed t-test.

±t24 at α= 0.01= ±2.797;

Because -2.797 <1.333<+2.797, therefore, H0 cannot be rejected.

为什么不是2.58?题目不是说符合正态分布?