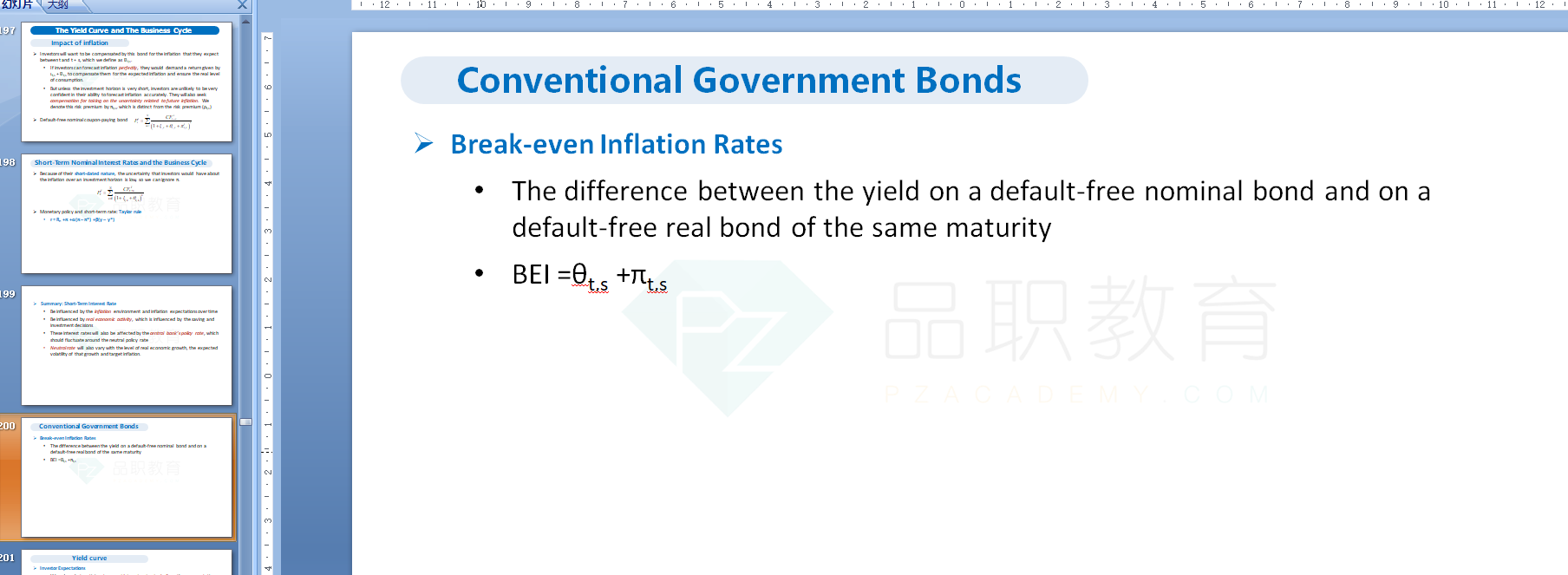

NO.PZ2018091701000021

问题如下:

The data in the following table is obtained by analyst using historical information:

The Analyst also manages to observe that the spread between the five-year default-free nominal bond and the default-free real zero-coupon bond in Country C is 2.35%, which of the following statement is correct?

选项:

A.expected rate of inflation is less than 2.35%.

B.expected rate of inflation is larger than 2.35%.

C.expected rate of inflation is equal to 2.35%.

解释:

A is correct.

考点:Breakeven inflation rates (BEI)

解析:the difference between the default-free nominal bond and the default-free real zero-coupon bond is BEI.

BEI=expected inflation rate + uncertainty of inflation rate. 不确定性即是风险,对于风险就有风险补偿,这样的补偿通常认为是正的,所以uncertainty of inflation rate>0.

因此当BEI=2.35%时, 而uncertainty of inflation rate>0,那么expected rate if inflation 小于2.35%。

能给我讲解一下吗