问题如下:

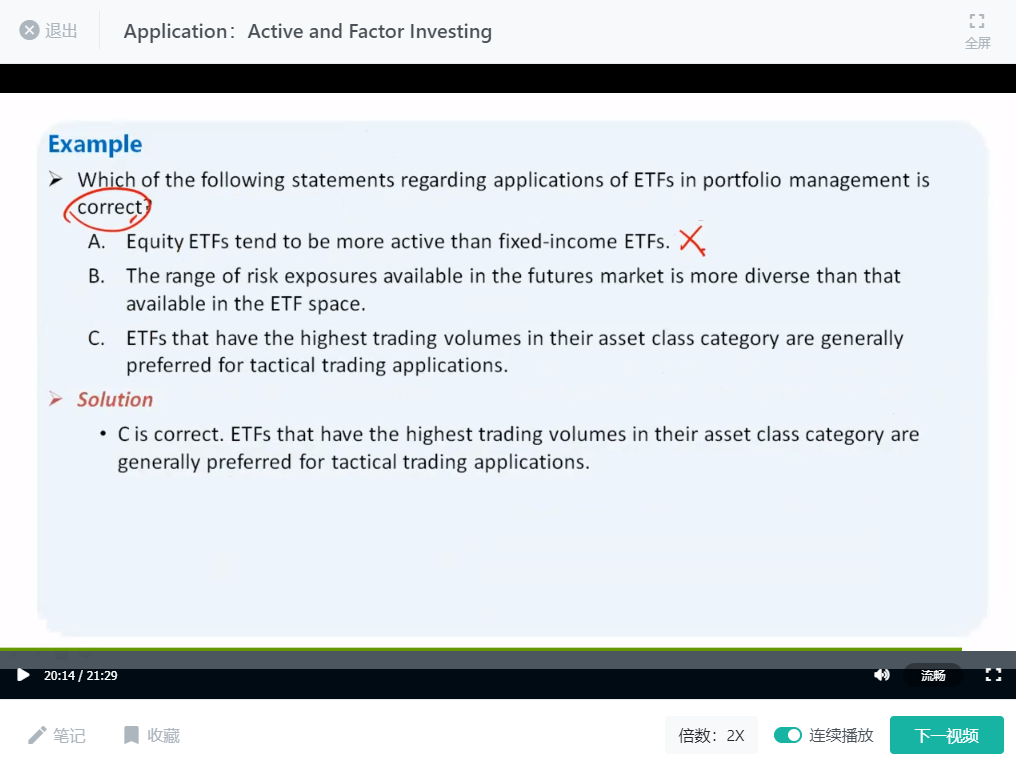

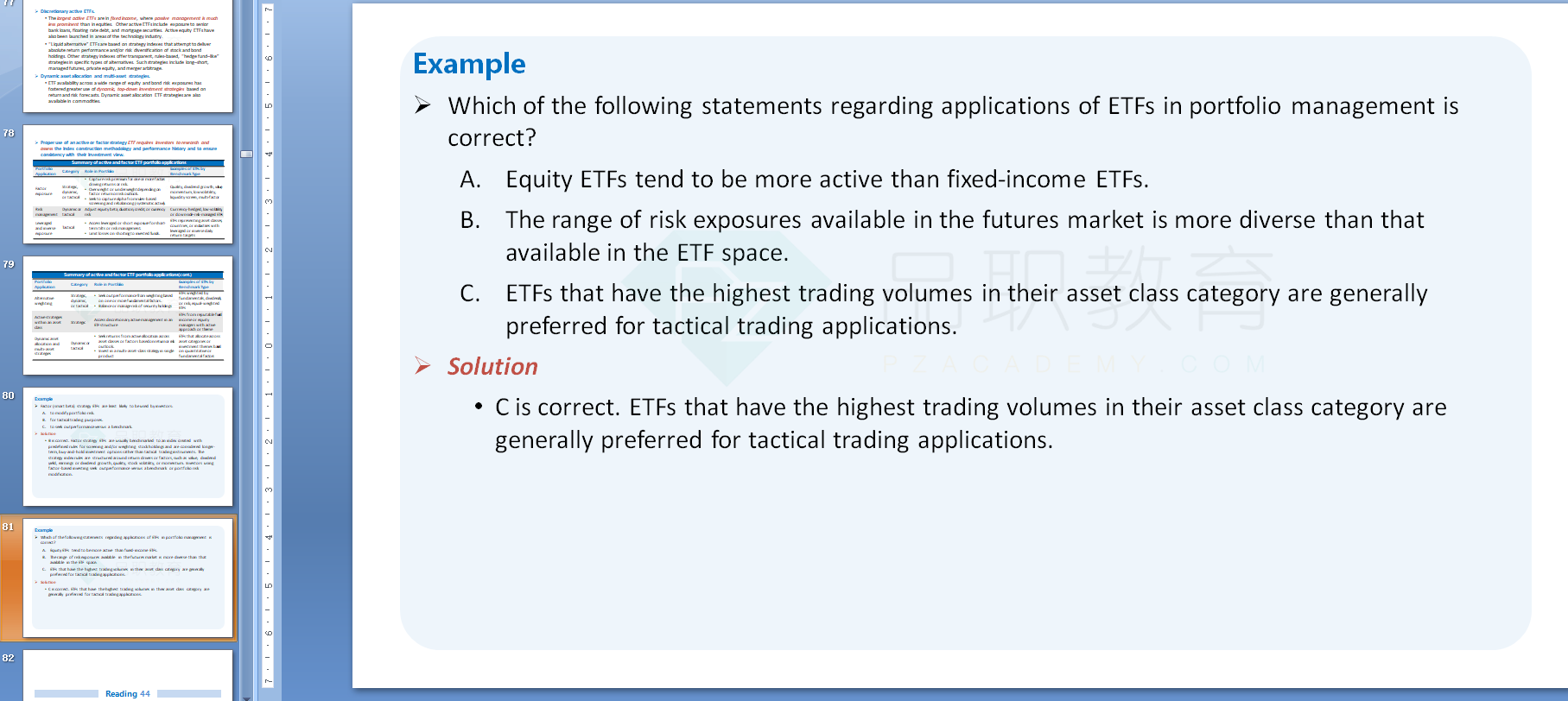

Which of the following statements regarding applications of ETFs in portfolio management is correct?

选项:

A. Equity ETFs tend to be more active than fixed-income ETFs.

B. The range of risk exposures available in the futures market is more diverse than that available in the ETF space.

C. ETFs that have the highest trading volumes in their asset class category are generally preferred for tactical trading applications.

解释:

C is correct. ETFs that have the highest trading volumes in their asset class category are generally preferred for tactical trading applications.

A为什么错,对比fixed income,equity不是更活跃,流动性更强嘛