NO.PZ2016082405000067

问题如下:

Based on the following information, what are the the risk-neutral and real-world default probabilities?

• Market price of bond is 92.

• Liquidity premium is 1%.

• Credit risk premium is 2%.

• Risk-free rate is 2.5%.

• Expected inflation is 1.5%.

• Recovery rate is 0%.

选项:

Risk-neutral probability

Real-world probability

5%

8%

8%

5%

6%

8%

5%

6%

解释:

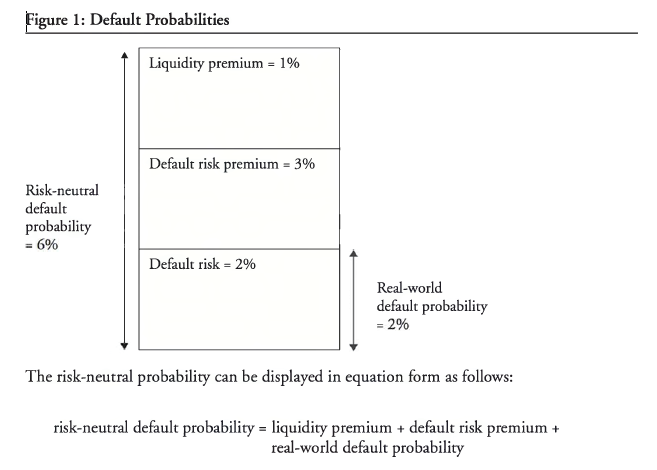

B The risk-neutral default probability is approximately 8% because the market price is 92% of par.

risk-neutral probability = real-world probability + credit risk premium + liquidity premium

8% = real-world probability + 2% + 1%

real-world probability = 8% - 3% = 5%

这里的real-world-PD,我理解用中性减掉LRP,但是为什么要减去CRP?CRP不是应该包括在真实世界PD里面吗?