NO.PZ201512300100000804

问题如下:

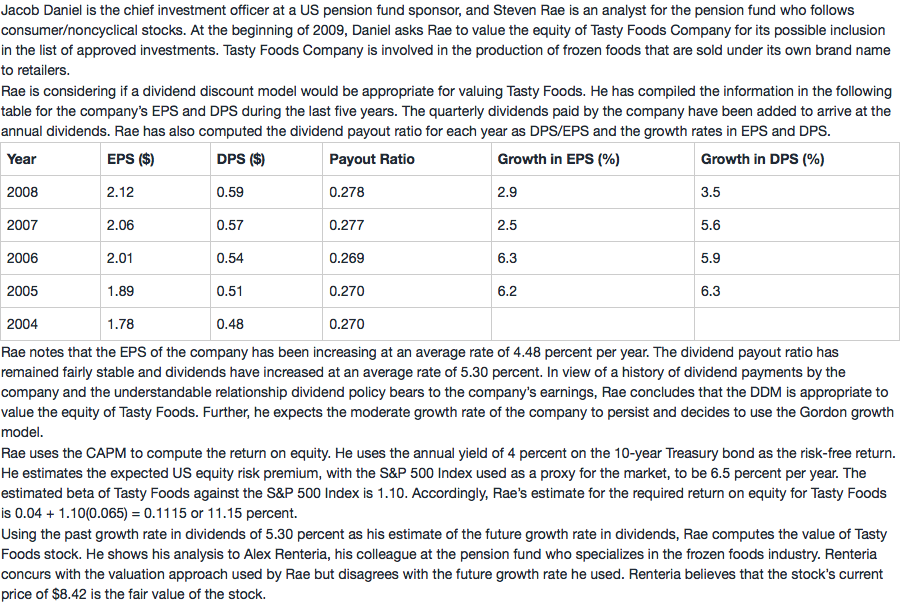

4. The beta of Tasty Foods stock of 1.10 used by Rae in computing the required return on equity was based on monthly returns for the last 10 years. If Rae uses daily returns for the last 5 years, the beta estimate is 1.25. If a beta of 1.25 is used, what would be Rae’s estimate of the value of the stock of Tasty Foods?

选项:

A.$8.64.

B.$9.10.

C.$20.13.

解释:

B is correct.

Using a beta of 1.25, Rae’s estimate for the required return on equity for Tasty Foods is 0.04 + 1.25(0.065) = 0.1213 or 12.13 percent. The estimated value of the stock is

$$V_0=\frac{D_1}{r-g}=\frac{0.59(1+0.0530)}{0.1213-0.0530}=\$9.10$$

就是文章里面的范例最后EAP也是Rm,而没有去减Rf,这是为什么啊,是出于什么考虑呢?