NO.PZ201702190300000408

问题如下:

8.The strategy suggested by Lee for hedging small moves in Soiomon‘s ETF position would most likely involve:

选项:

A. selling put options.

B. selling call options.

C. buying call options.

解释:

B is correct

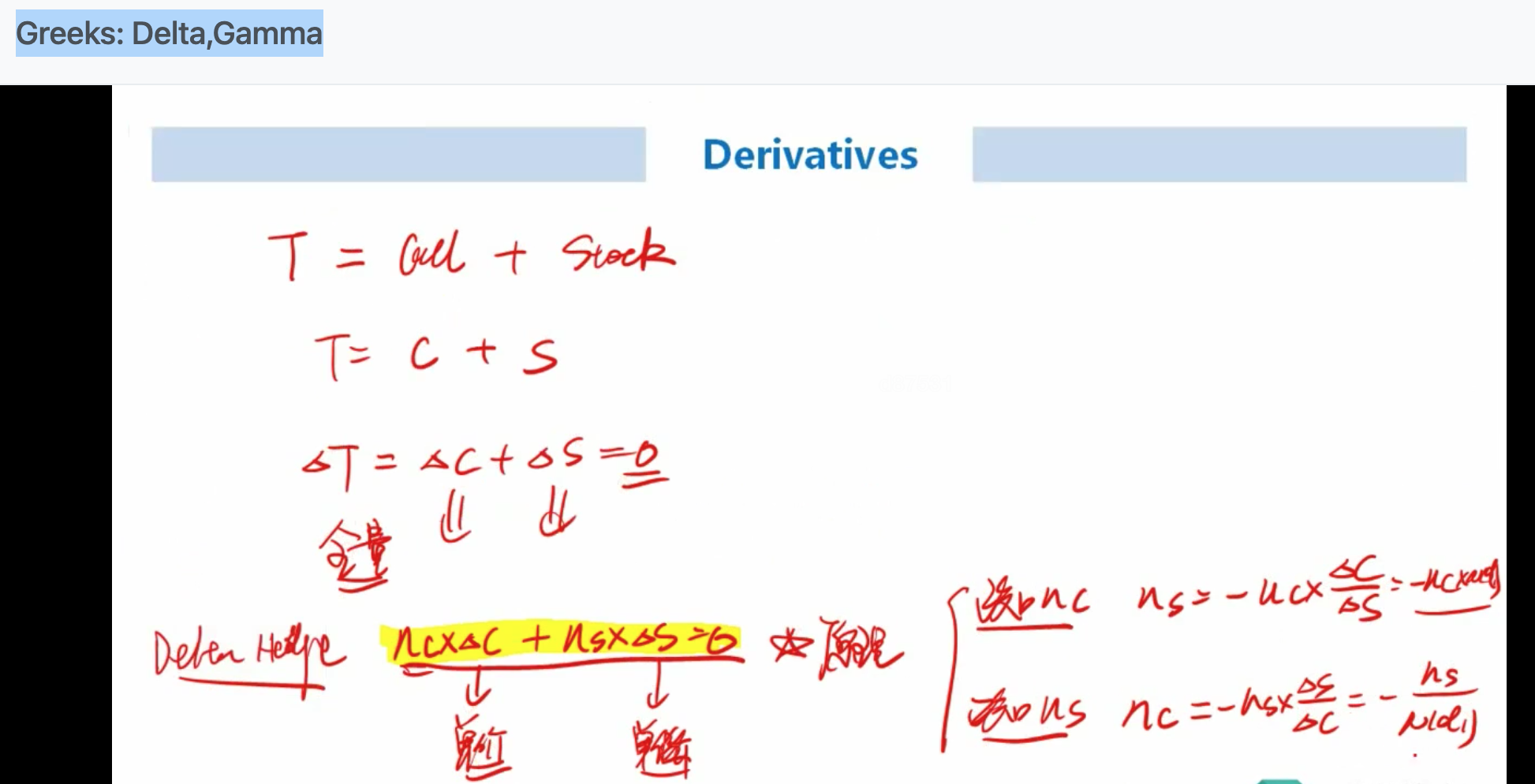

because selling call options creates a short position in the ETF that would hedge his current long position in the ETF.

Exhibit 2 could also be used to answer the question. Solomon owns 10,000 shares of the GPX, each with a delta of +1; by definition, his portfolio delta is + 10,000. A delta hedge could be implemented by selling enough calls to make the portfolio delta neutral:

1,解析中的公式从哪里来的?我在强化班中并没有看到。为什么可以直接用 portfolio delta除以 delta put ,而且分子分母都是正数,得出来的是负数? 2.怎么定量求解?