NO.PZ2017092702000029

问题如下:

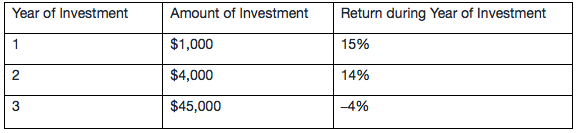

A fund receives investments at the beginning of each year and generates returns as shown in the table.

Which return measure over the three-year period is negative?

选项:

A.Geometric mean return

B.Time-weighted rate of return

C.Money-weighted rate of return

解释:

C is correct.

The money-weighted rate of return considers both the timing and amounts of investments into the fund. The investment at the beginning of Year 1 will be worth $1,000(1.15)(1.14)(0.96) = $1,258.56 at the end of Year 3. The investment made at the beginning of Year 2 will be worth $4,377.60 = $4,000(1.14)(0.96) at the end of Year 3. The investment of $45,000 at the beginning of Year 3 decreases to a value of $45,000 (0.96) = $43,200 at the end of Year 3. Solving for r,

results in r = –2.08%

Note that B is incorrect because the time-weighted rate of return (TWR) of the fund is the same as the geometric mean return of the fund and is thus positive: TWR = √ 3 (1.15) (1.14) (0.96) - 1 = 7.97%

先清空计算器,然后输入CF0 = –$1,000, CF1 = –$2,850, F1=1,CF2 = –$40,440, F2=1,CF3 = +$43,200,F3=1,IRR enter

为啥不是CF0 = –$1,000,CF1=-4000,CF2 = 3836.16?

3836.16=-45000+ 48836.16(第三年投入的钱-第三年收到的钱=第三年股东实际拿到的钱)

【(1000*1.15+4000)】*1.14+45000}*(1-4%)=48836.16(这三年赚的钱)