问题如下:

Let X be a random variable representing the daily loss of your portfolio. The "peaks over threshold" (POT) approach considers a threshold value, u, of X and the distribution of excess losses over this threshold. Which of the following statements about this application of extreme value theory is correct?

选项:

A.

To apply the POT approach, the distribution of X must be elliptical and known.

B.

If X is normally distributed, the distribution of excess losses requires the estimation of only one parameter, β, which is a positive scale parameter.

C.

To apply the POT approach, one must choose a threshold, u, which is high enough that the number of observations in excess of u is zero.

D.

As the threshold, u, increases, the distribution of excess losses over u converges to a generalized Pareto distribution.

解释:

D is correct.

考点: Extreme Value

解析: The distribution of excess losses over u converges to a generalized Pareto distribution as the threshold value u increases.

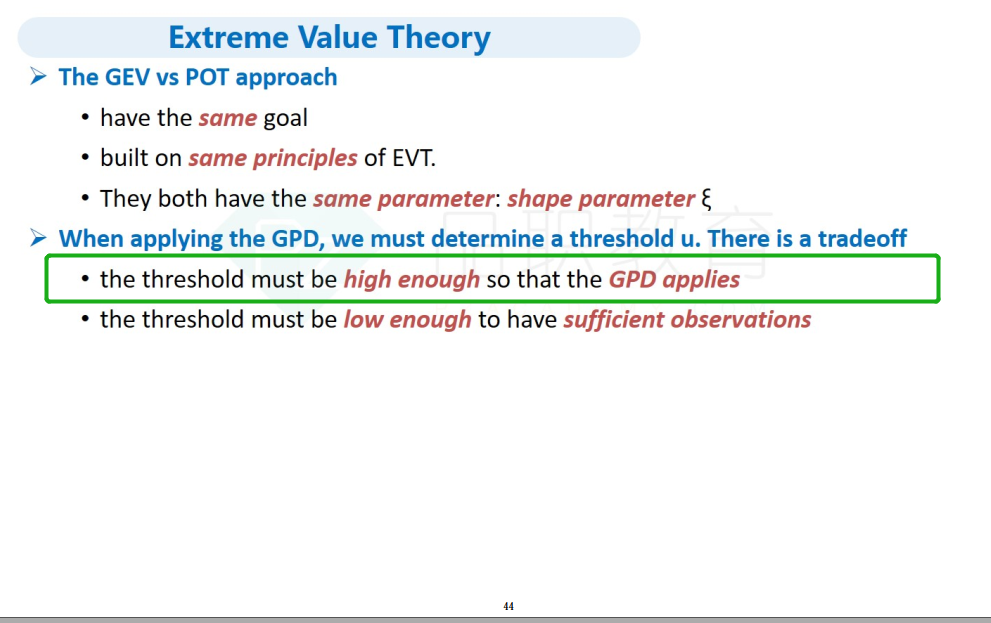

The distribution of X itself can be any of the commonly used distribution: normal, lognormal, t, etc., and will usually be known. The distribution of excess losses requires the estimation of two parameters, a positive scale parameter β and a shape or tail index parameter ξ. One must choose a threshold u that is high enough so that the theory applies but also low enough so that there are observations in excess of u.

n增大,POT不是更趋近于广义极值理论吗?POT本身就是广义帕累托,怎么能说趋近呢?