问题如下:

During the 2007-2009 global financial crisis, traders and risk managers used copula to model correlations, but the models and the economy actually differed greatly, which also led to incorrect estimates of structured product risks , Which of the following statements is the least likely to explain the failure of the copula model during the financial crisis?

选项:

A.During the financial crisis, correlations for senior tranches of CDOs stays constant.

B.The copula correlation model was calibrated using data from low-risk time periods..

C.During the financial crisis, correlations for both equity and mezzanine tranches of CDOs increased.

D.The copula correlation model assumes that the CDO equity tranche and senior tranche are negatively correlated.

解释:

A is correct.

考点:copula function

解析:金融危机时,整个环境都在恶化,各个senior层内的违约情况也都在增高,senior层之间的correlation也在上升。

老师好,一共有三个问题:

1、这道题的C选项的意思,是不是指的是在financial crisis时,equity tranch和mezzanine tranch各自内部的相关系数增加?而不是指equity tranch和mezzanine tranch两个层级之间的相关系数变大?

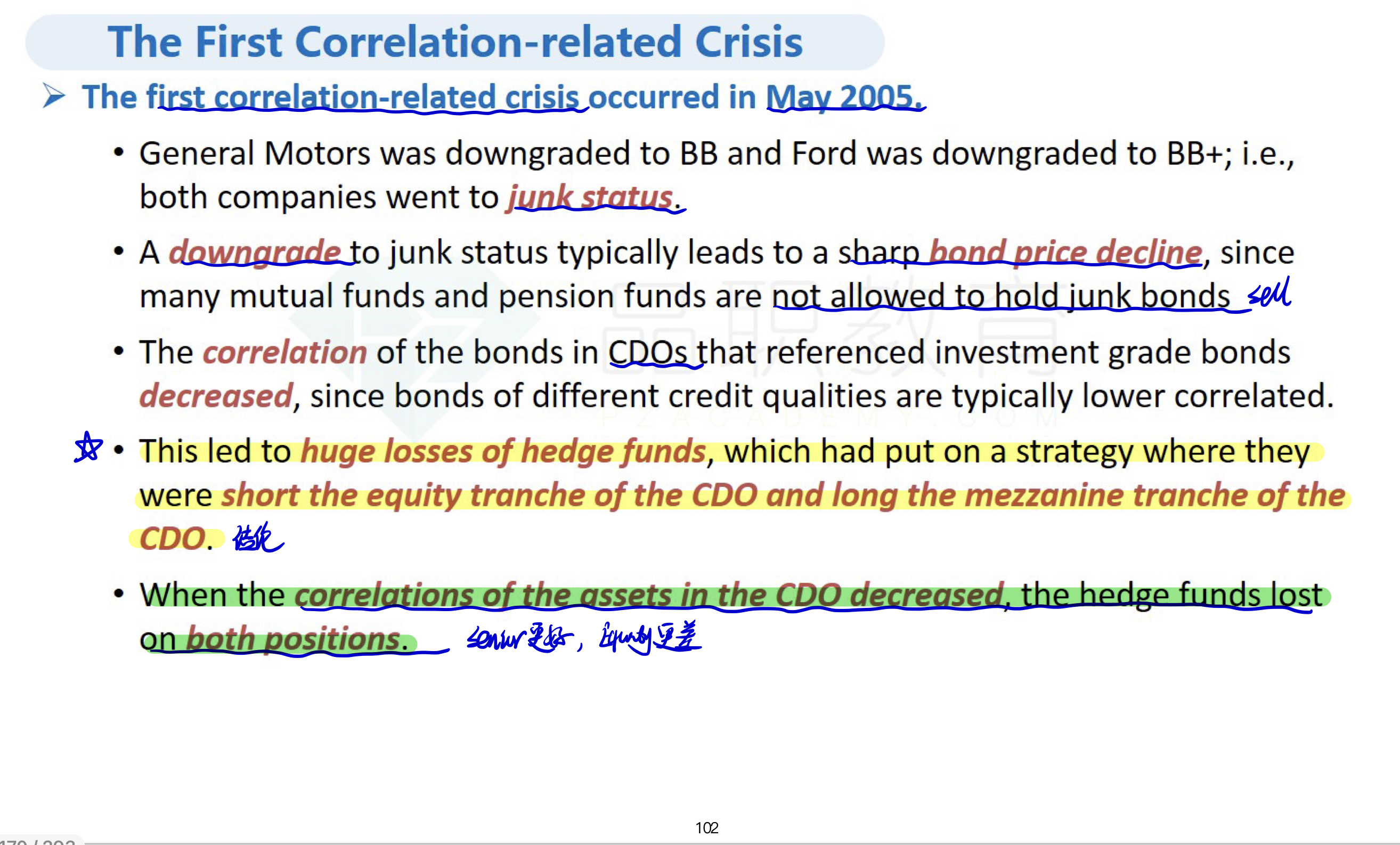

2、另外,基础班讲义第102页和第104页标绿色的句子(下图),指的是equity tranch和mezzanine tranch两个层级之间的相关系数变小,而不是各自内部的相关系数变小?

3、还有就是基础班讲义里面的这个2005年的危机案例是个特例,一般情况下,危机时,相关系数是变大的,但是这个案例是变小?