问题如下:

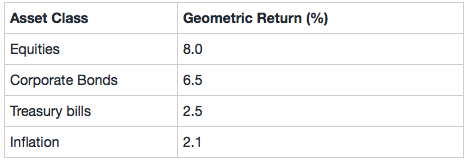

An analyst observes the following historic geometric returns:

The risk premium for corporate bonds is closest to:

选项:

A.3.5%

3.9%

4.0%

解释:

B is correct. (1 + 0.0650)/(1 + 0.0250) – 1 = 3.9%

请问这道题。我的这个方法问题出在哪里?这样计算出来的结果不对。

(1+Rf+risk-perimue)*(1+inflation rate)=1+ corpotate bond rate