问题如下:

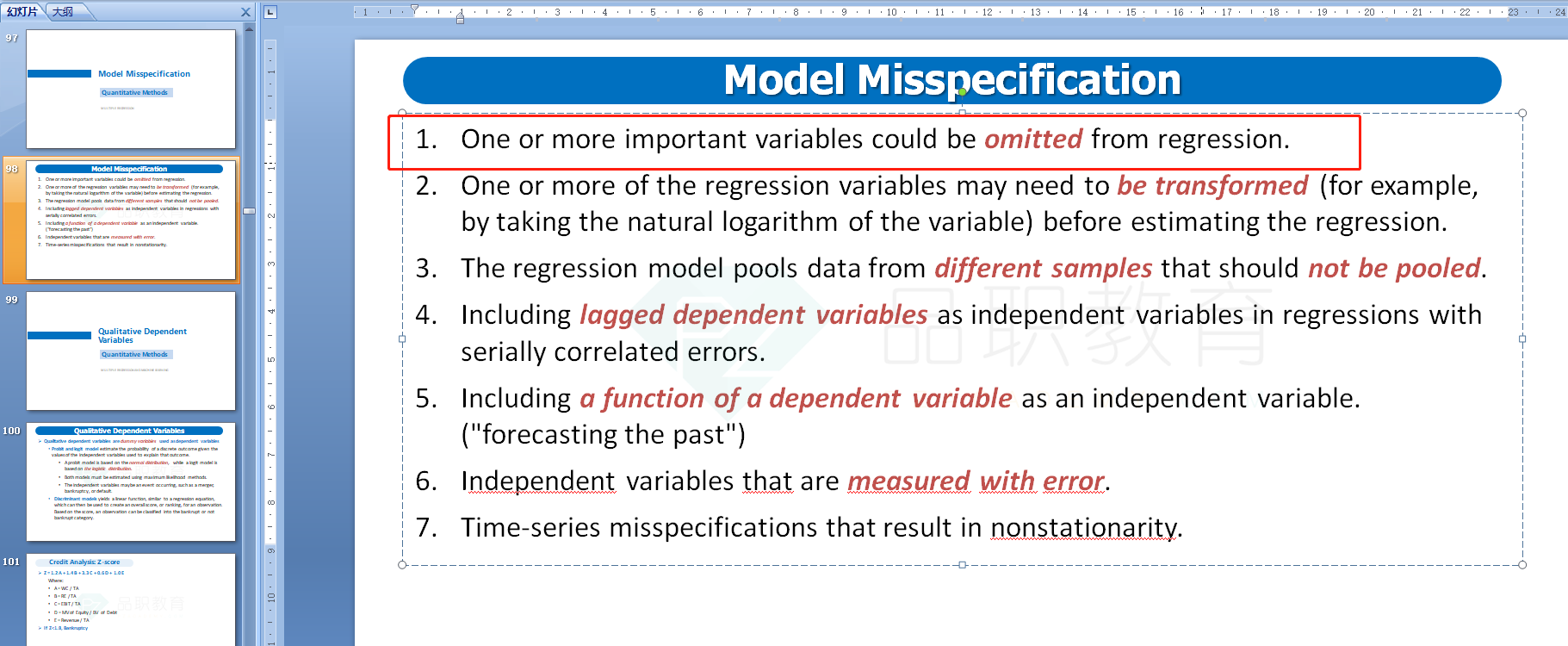

If an omitted variable is correlated with variables already included in the model, coefficient estimates will be biased and inconsistent and standard errors will also be inconsistent. Is this Statement correct?

选项:

A. Yes.

B. No, because the model’s coefficient estimates will be unbiased.

C. No, because the model’s coefficient estimates will be consistent.

解释:

A is correct.

Chang is correct because a correlated omitted variable will result in biased and inconsistent parameter estimates and inconsistent standard errors.

对应讲义在哪里?谢谢