问题如下:

1.Based on Exhibit 1 and assuming annual compounding, the arbitrage profit on the bond futures contract is closest to:

选项:

A.0.4158

B.0.5356

C.0.6195

解释:

B is correct.

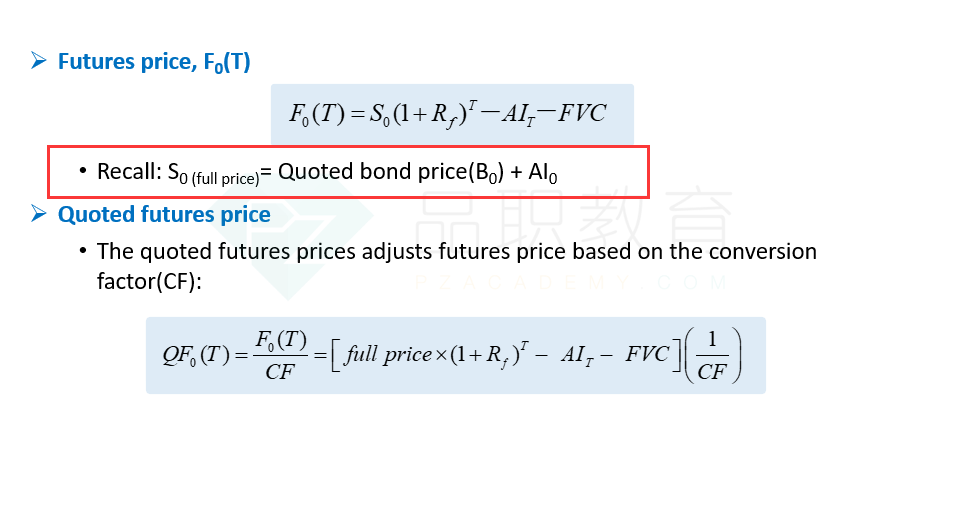

The no-arbitrage futures price is equal to the following:

F0(T) = FV0,T(T)[B0(T + Y) + Al0 – PVCI0,T]

F0(T) = (1 + 0.003)0.25(112.00 + 0.08 - 0)

F0(T) = (1 + 0.003)0.25 (112.08) = 112.1640

The adjusted price of the futures contract is equal to the conversion factor multiplied by the quoted futures price:

F0(T)=CF(T)QF0(T)

F0(T) = (0.90)(125) = 112.50

Adding the accrued interest of 0.20 in three months (futures contract expiration) to the adjusted price of the futures contract gives a total price of 112.70.

This difference means that the futures contract is overpriced by 112.70 - 112.1640 = 0.5360. The available arbitrage profit is the present value of this difference: 0.5360/(1.003)0.25 = 0.5356.

此处的0.08应计利息不是应该包含在112的债券报价里的吗?相当于如果没有应计利息,债券报价应该是112-0.08=111.92

为何此处0.08是在112之外额外的一笔利息啊?