Q. Which of the following statements regarding Macaulay duration is correct?

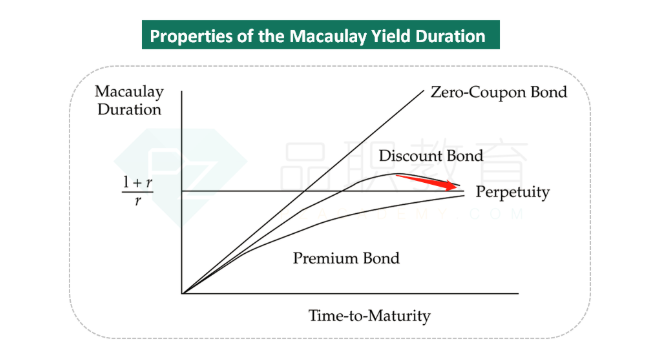

- For a given coupon rate, Macaulay duration can be lower for a long-term discount bond than for a short-term discount bond.

- For a given time to maturity and yield to maturity, Macaulay duration is lower for a zero-coupon bond than for a low-coupon bond trading at a discount.

- For a given time to maturity and yield to maturity, Macaulay duration is lower for a low-coupon bond trading at a discount than for a high-coupon bond trading at a premium.

老师,不是期限越长Mac Duration越大吗?谢谢