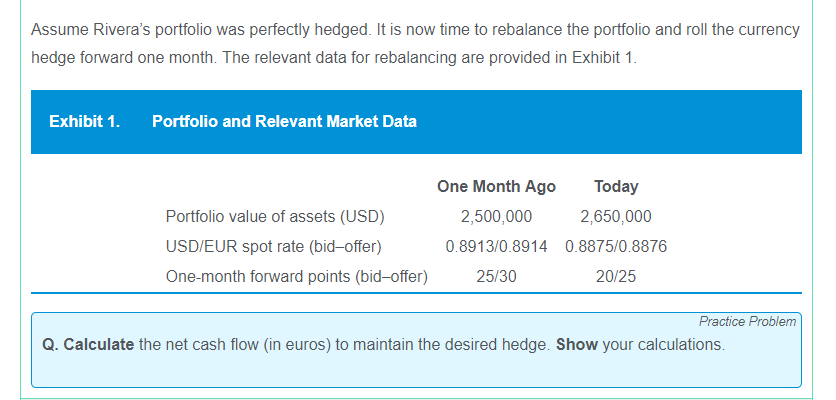

When hedging one month ago, Delgado would have sold USD2,500,000 one month forward against the euro. Now, with the US dollar-denominated portfolio increasing in value to USD2,650,000, a mismatched FX swap is needed to settle the initial expiring forward contract and establish a new hedge given the higher market value of the US dollar-denominated portfolio.

To calculate the net cash flow (in euros) to maintain the desired hedge, the following steps are necessary:

- Buy USD2,500,000 at the spot rate. Buying US dollars against the euro means selling euros, which is the base currency in the USD/EUR spot rate. Therefore, the bid side of the market must be used to calculate the outflow in euros.

- USD2,500,000 × 0.8875 = EUR2,218,750.

- Sell USD2,650,000 at the spot rate adjusted for the one-month forward points (all-in forward rate). Selling the US dollar against the euro means buying euros, which is the base currency in the USD/EUR spot rate. Therefore, the offer side of the market must be used to calculate the inflow in euros.

- All-in forward rate = 0.8876 + (25/10,000) = 0.8901.

- USD2,650,000 × 0.8901 = EUR2,358,765.

- Therefore, the net cash flow is equal to EUR2,358,765 – EUR2,218,750, which is equal to EUR140,015.