问题如下:

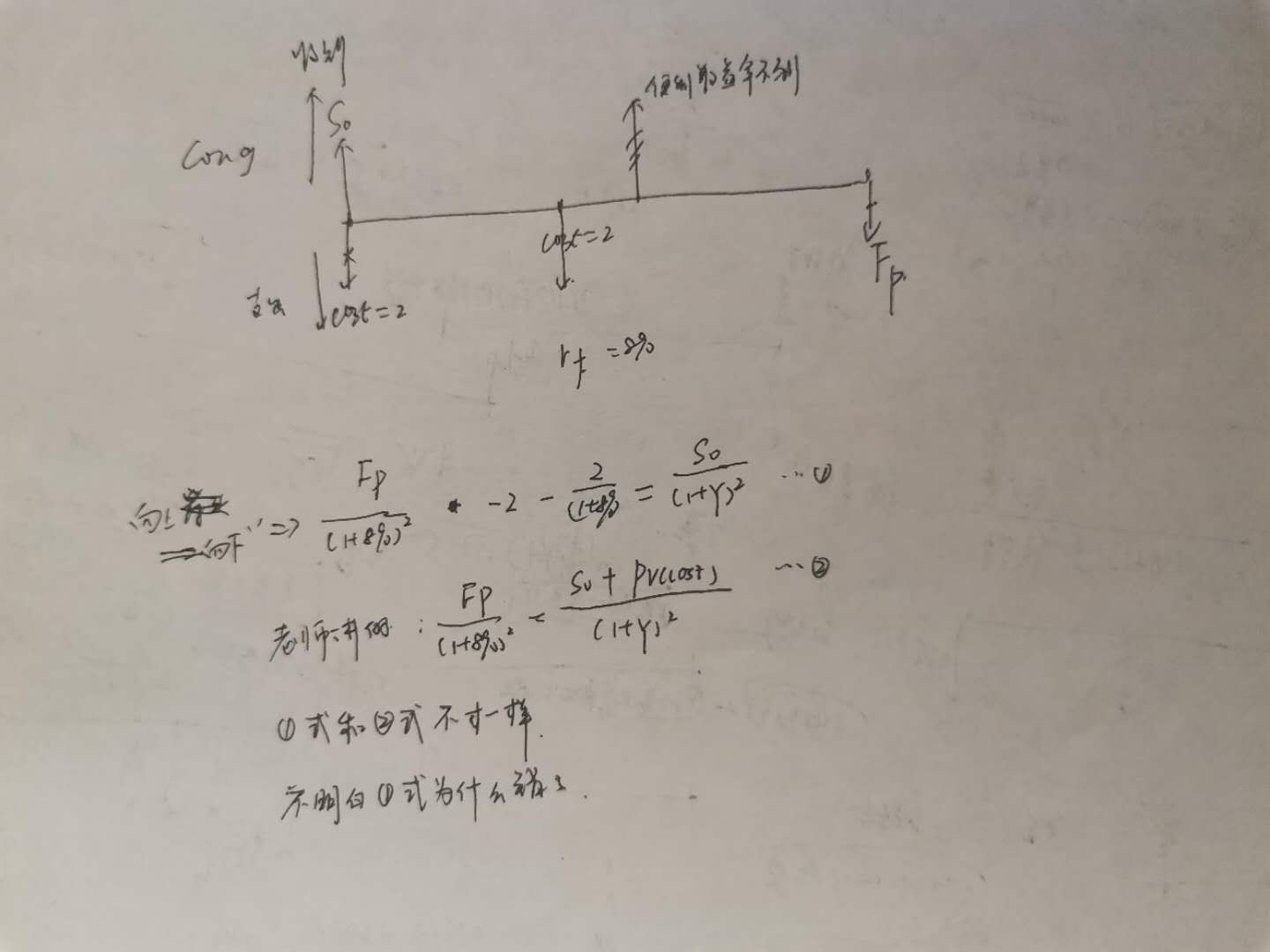

Suppose that the storage costs for crude oil are USD 2 per barrel per year payable at the beginning of the year. The current spot price is USD 75, and the two-year futures price is USD 72. The risk-free interest rate is 8% per annum (compounded annually). Estimate the convenience yield of crude oil per year.

选项:

解释:

The present value of the storage costs per barrel over two years is

2 + 2/ 1.08 = 3.85

The convenience yield Y is given by solving:

The solution is

that is, the convenience yield is about 13% per year.