问题如下:

The following statements are about using

the duration to hedge against interest rate risk, which of the following is NOT

correct?

选项:

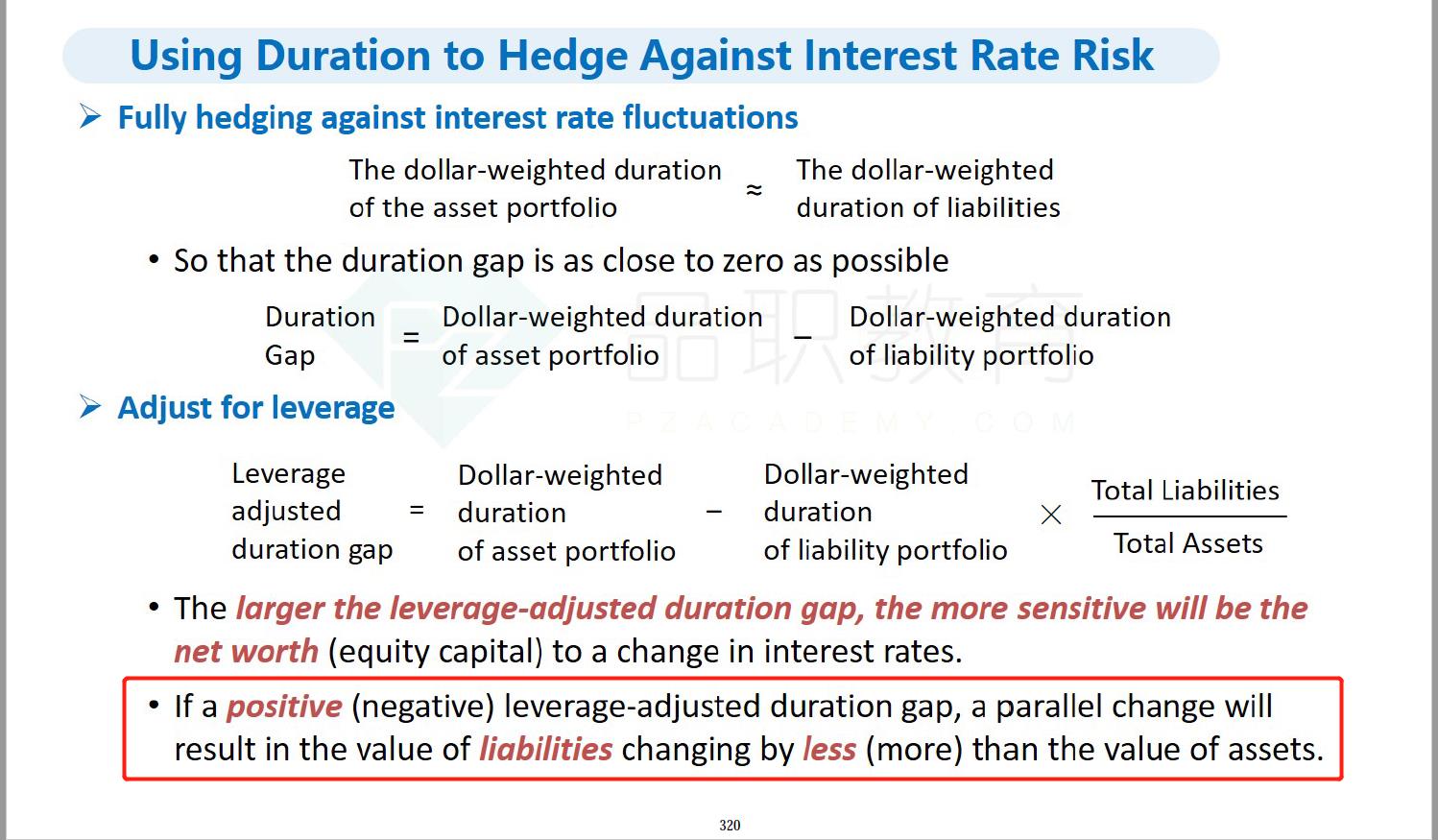

A. The larger the

leverage-adjusted duration gap, the more sensitive will be the net worth

(equity capital) to a change in interest rates.

If a positive (negative)

leverage-adjusted duration gap, a parallel change will result in the value of

liabilities changing by less (more) than the value of assets.

Duration gap = dollar-weighted duration of

asset portfolio – dollar weighted duration of liability portfolio

Leverage

adjusted duration gap = dollar-weighted duration of asset portfolio – dollar

weighted duration of liability portfolio × Total asset

/ equity

解释:

考点:对Risk Management for Changing Interest

Rates: ALM and Duration Techniques-The Concept of Duration as a Risk-Management

Tool的理解

答案:D

解析:

D选项Leverage

adjusted duration gap的公式错误,正确的公式为:

Leverage adjusted duration gap =

dollar-weighted duration of asset portfolio – dollar weighted duration of

liability portfolio × Total liabilities/ Total Assets

老师亲吻一下B是怎么判断的,只记得上课的时候老实说,D>0,利率上升,E 下降;这里说平行移动,如果D>0...后面资产变得比负债多,没说方向嘛,怎么弄呢这里