问题如下:

Which of the following statements best describes the calculation of implied correlation?

选项:

A.The implied correlation for the mezzanine tranche assumes non-constant pairwise correlation.

B.Observable market prices of credit default swaps are used to infer the tranche values.

C.The tranche pricing function is calibrated to match the model price with the market price.

D.The risk-adjusted default probabilities are used in model calibration.

解释:

C Starting with observed market prices and a pricing function for the tranches, it is possible to back out the implied correlation to calibrate the model price with the market price. The computation of implied correlation assumes constant pairwise correlation. Both credit default swap and tranche values are observed. Observed tranche values are used in conjunction with risk-neutral default probabilities to compute implied correlation.

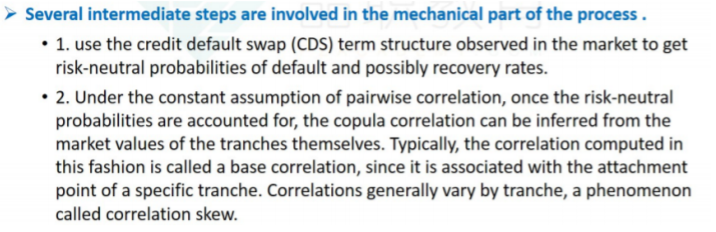

老师理解不了第二点,什么是pariwise correlation,为什么在pariwise correlation的情况下,从风险中性触发,可以用coupla函数可高出tranches 之间的相关关系,后边那个base correlation又是啥,correlation skew又是啥,上课哪里没有讲的很清楚感觉

老师理解不了第二点,什么是pariwise correlation,为什么在pariwise correlation的情况下,从风险中性触发,可以用coupla函数可高出tranches 之间的相关关系,后边那个base correlation又是啥,correlation skew又是啥,上课哪里没有讲的很清楚感觉