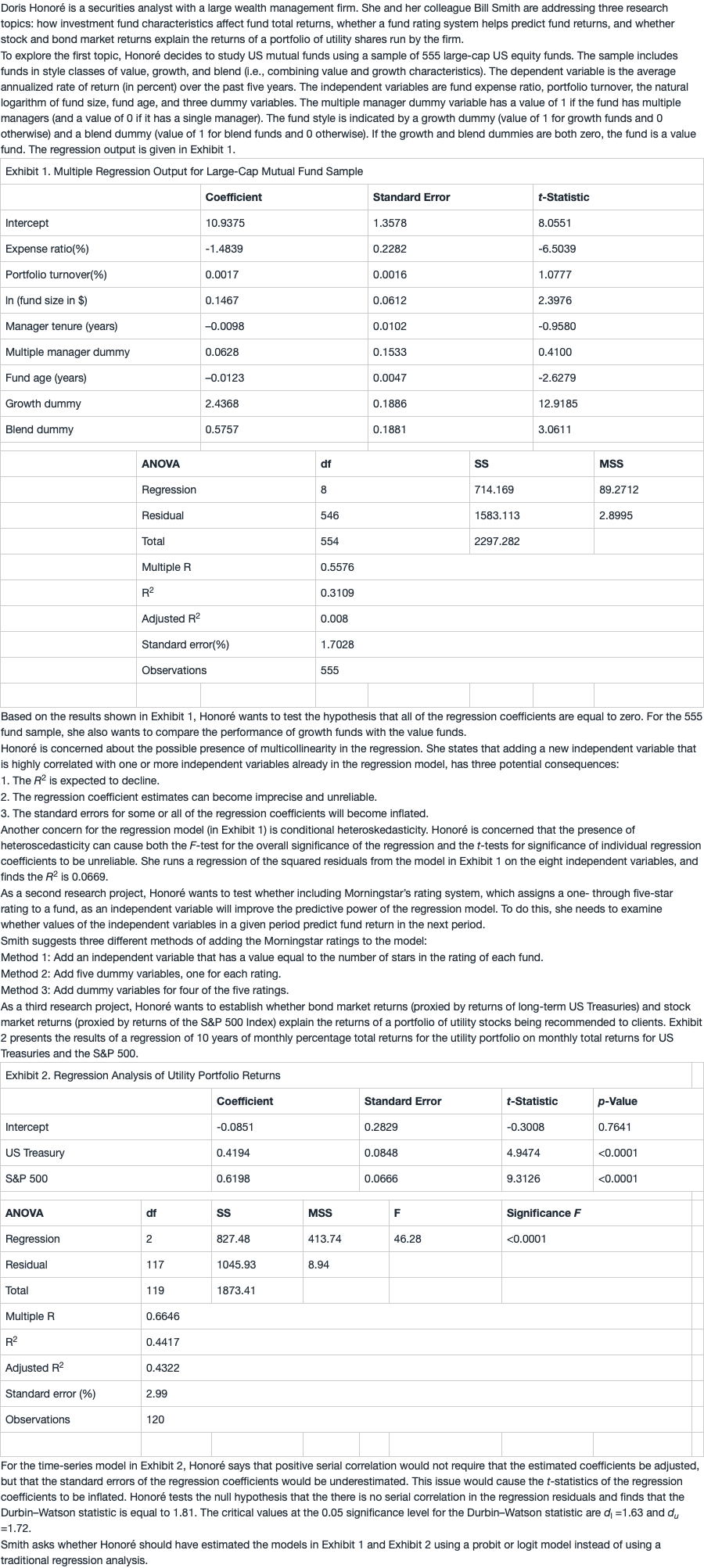

问题如下:

8. Should Honoré have estimated the models in Exhibit 1 and Exhibit 2 using probit or logit models instead of traditional regression analysis?

选项:

A.Both should be estimated with probit or logit models.

B.Neither should be estimated with probit or logit models.

C.Only the analysis in Exhibit 1 should be done with probit or logit models.

解释:

B is correct. Probit and logit models are used for models with qualitative dependent variables, such as models in which the dependent variable can have one of two discreet outcomes (i.e., 0 or 1). The analysis in the two exhibits are explaining security returns, which are continuous (not 0 or 1) variables.

老师好 一般什么情况下要用probit and logit models?谢谢