问题如下:

What is the formula for the expected return (with continuous compounding) over a time period of T when the Black-Scholes-Merton assumptions are made?

选项:

解释:

The expected return is

. (This does not depend on T.)

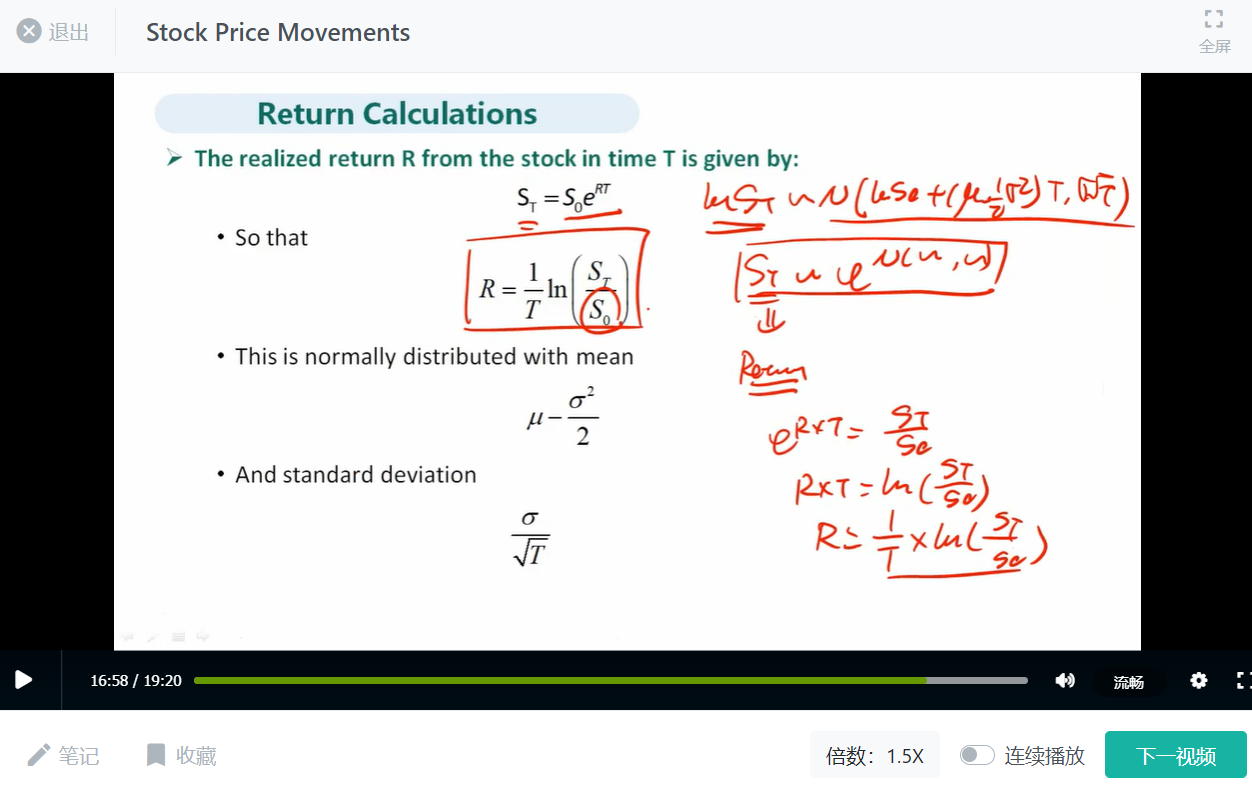

stock price movements里有2个expected return

一个是 stock的平均回报,(s1-s0)/s1;对应均值是μ

另一个是return的平均值,ln(s1/S0),对应均值就是μ-0.5*σ^2

请教,做题时如何区分。