问题如下:

An investor evaluating the returns of three recently formed exchange-traded funds gathers the following information:

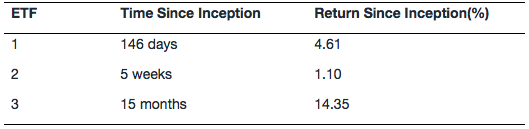

The ETF with the highest annualized rate of return is:

选项:

A.ETF 1.

B.ETF 2.

C.ETF 3.

解释:

B is correct.

The annualized rate of return for ETF 2 is 12.05% = (1.0110 )-1, which is greater than the annualized rate of ETF 1, 11.93% = (1.0461 )-1, and ETF 3, 11.32% = (1.1435 )-1. Despite having the lowest value for the periodic rate, ETF 2 has the highest annualized rate of return because of the reinvestment rate assumption and the compounding of the periodic rate.

请问一年什么时候看做365,什么时候看做360?以及annualized rate就是EAR吗?我记得EAR是真实的年利率,那还有个假的年利率是什么?