问题如下:

Provide an alternative decomposition of the chooser option to that given in the chapter so that it is a call maturing at time T1 plus a put maturing at time T2 .

选项:

解释:

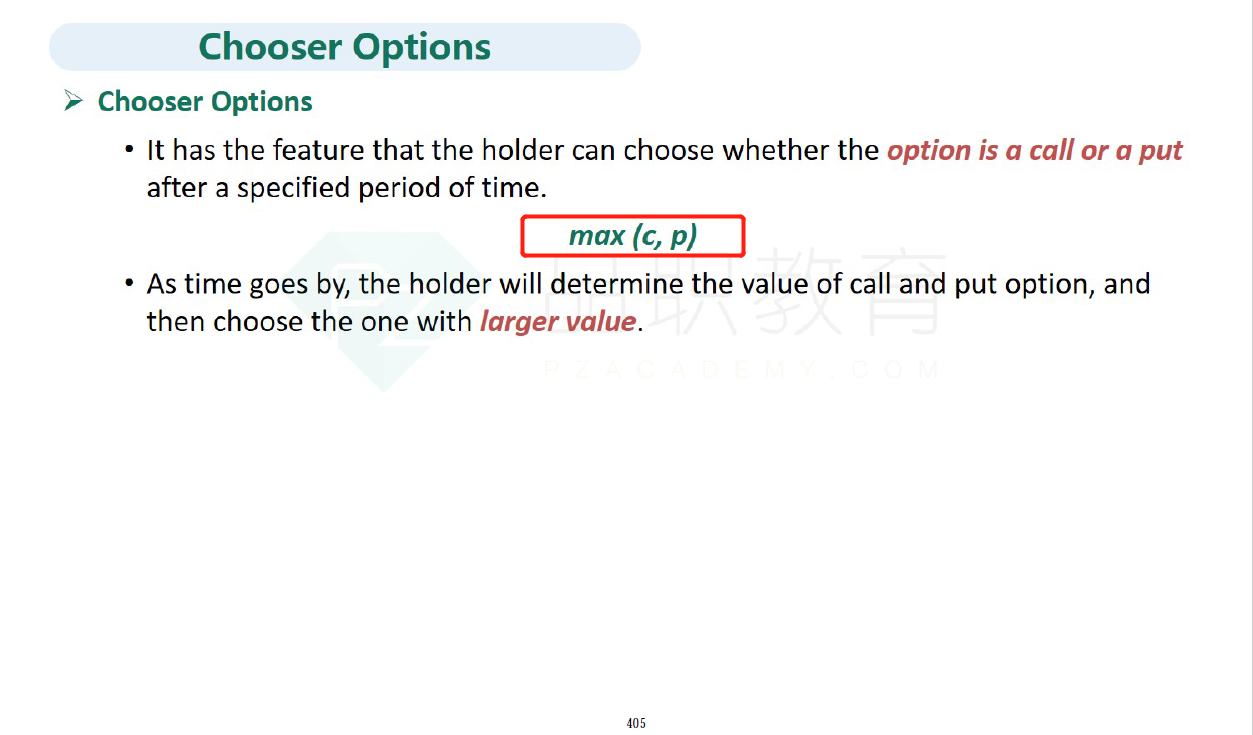

With the notation in the text we can write max(c, p) = p + max(c - p, 0) = p + max(S - PV(K), 0)

This shows that the chooser option is a portfolio consisting of:

• A put option maturing at time T2, and

• A call option with strike price PV(K) maturing at time T1.

请问第一步Max(C,P)怎么退出来的?