问题如下:

Which of the following statements would least likely describe an appropriate use of a security market index?

选项:

A. Reflections of market sentiment.

B. Comparing a value manager's performance against a broad market index.

C. Proxies for measuring of beta and risk-adjusted return.

解释:

B is correct.

The index stocks are those that the manager actually choose from, which means that portfolio securities will be selected from value stocks. So a value manager should be compared against a value index, not a broad market index.

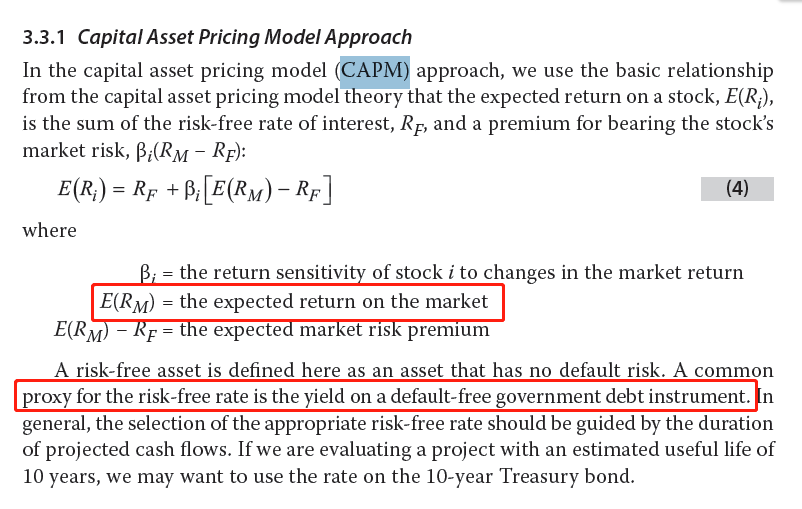

所以大盘指数指rf吗? R=rf +b(rm-rf) 我不太明白大盘指数和b的关系?????? 其次,跑赢大盘我们就认为基金经理的表现是不错的,为什么还要去考虑风格? 在讲义中很明显有这一条,老师上课的时候也说了:manger的业绩与大盘相比较 risk-adjusted return指的是调整过风险的收益,应该就是rf吧