问题如下:

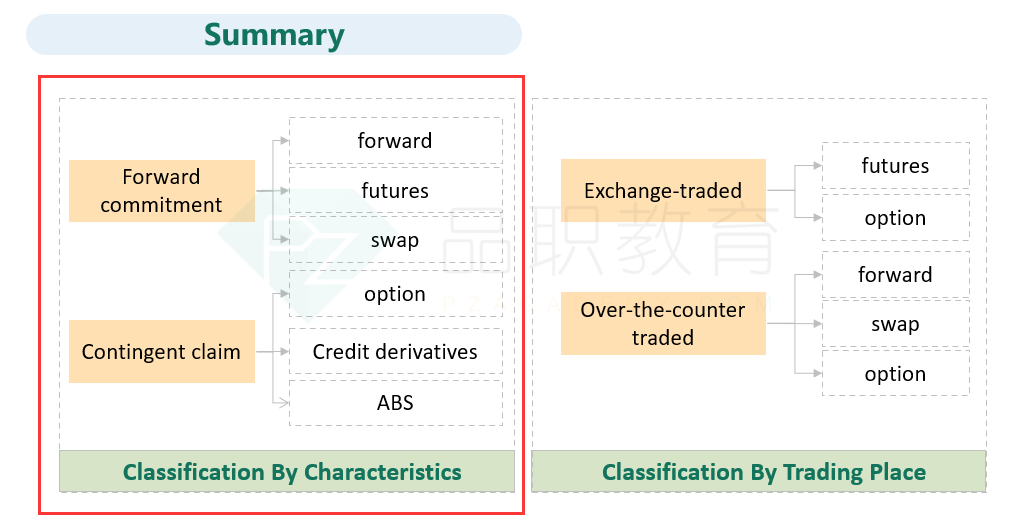

Which of the following derivatives is classified as a contingent claim?

选项:

A. Futures contracts

B. Interest rate swaps

C. Credit default swaps

解释:

C is correct.

A credit default swap (CDS) is a derivative in which the credit protection seller provides protection to the credit protection buyer against the credit risk of a separate party. CDS are classified as a contingent claim.

A is incorrect because futures contracts are classified as forward commitments. B is incorrect because interest rate swaps are classified as forward commitments.

请问B为什么不是呢?