丹丹_品职答疑助手 · 2020年08月31日

嗨,从没放弃的小努力你好:

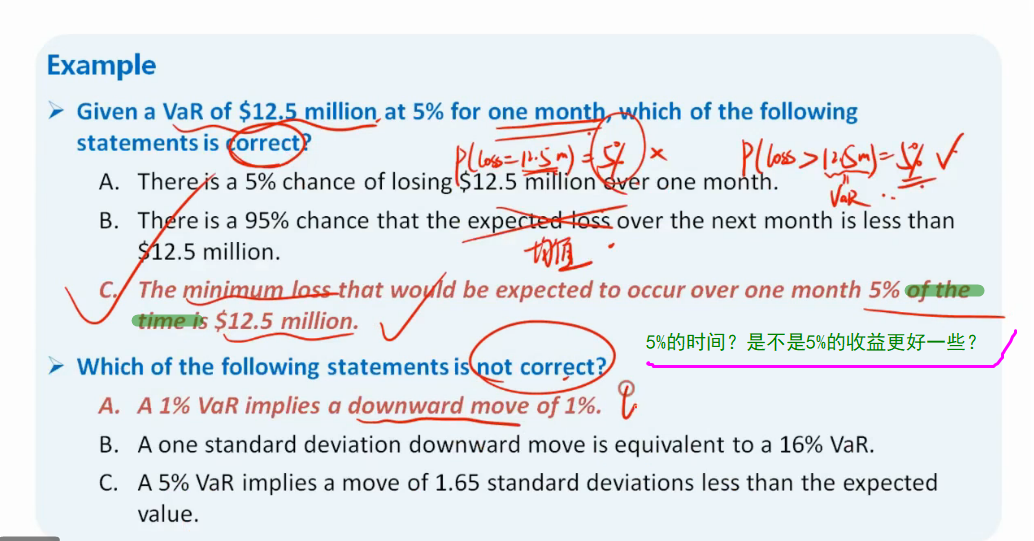

同学你好,从时间的角度是没问题的,我们考试也可能会考到,原版书也有相关知识点

A VaR statement references a time horizon: losses that would be expected to

occur over a given period of time. In this example, that period of time is one

day. (If VaR is measured on a daily basis, and a typical month has 20–22 business days, then 5% of the days equates to about one day per month.)

-------------------------------

努力的时光都是限量版,加油!