问题如下:

7.Based on Exhibits 2 and 3, and assuming annual compounding, the per share value of Troubadour’s short position in the TSI forward contract three months after contract initiation is closest to:

选项:

A.$1.6549.

B.$5.1561.

C.$6.6549.

解释:

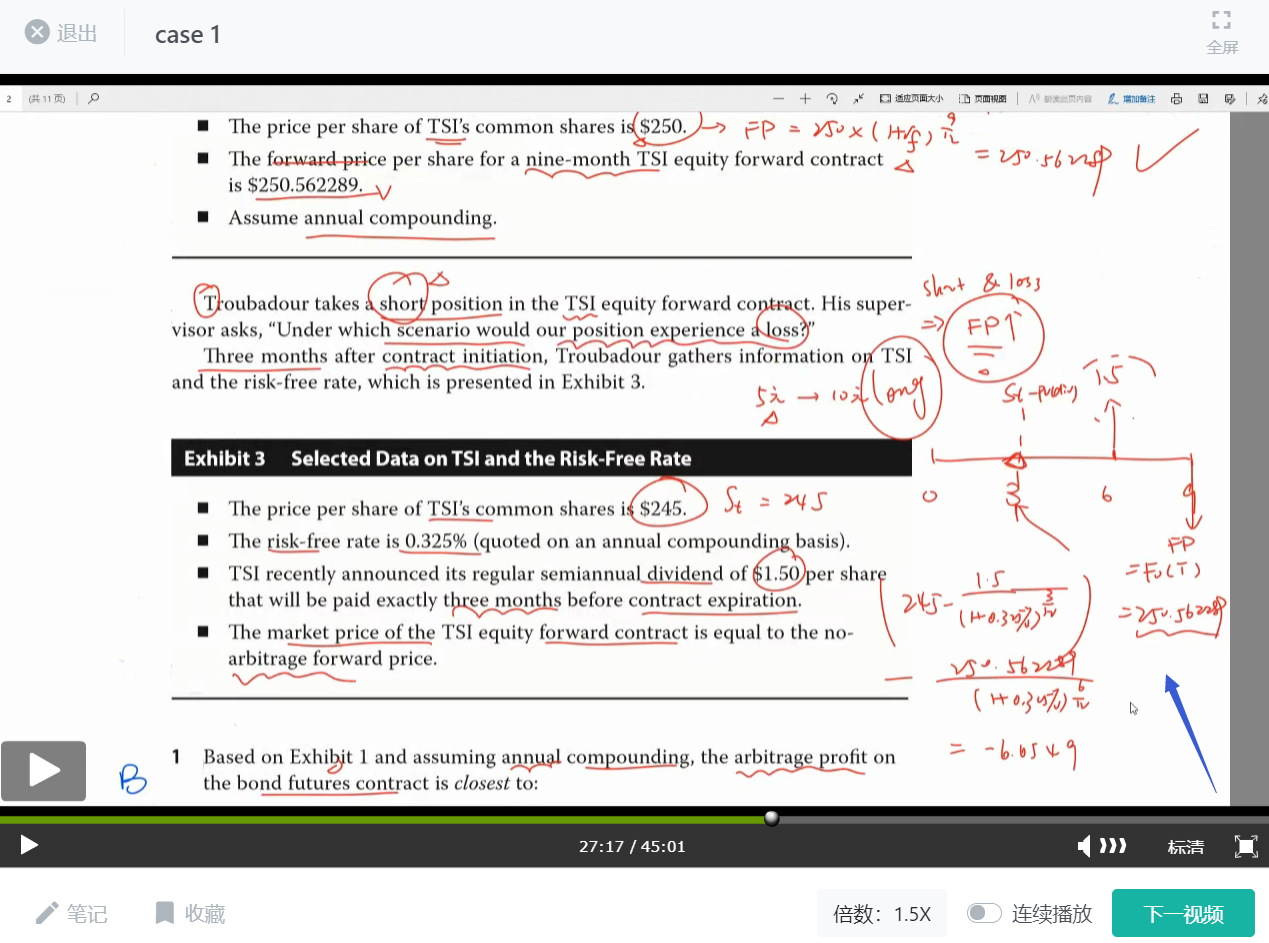

C is correct.

The no-arbitrage price of the forward contract, three months after contract initiation, is

F0.25(T) = FV0.25,T(S0.25 + θ.25 –γ0.25)

F0.25(T) = [$245 + 0 - $1.50/(1 + 0.00325)(0.5 - 0.25)](1 + 0.00325)(0.75 -0.25) = $243.8966

Therefore, from the perspective of the long, the value of the TSI forward contract is

V0.25(T)=PV0.25,T [F0.25(T) – F0(T)]

V0.25(T) = ($243.8966- $250.562289)/(1 + 0.00325)0.75 - 0.25 =-$6.6549

Because Troubadour is short the TSI forward contract, the value of his position is a gain of $6.6549.

老师可以请你用画图法不是重新定价法解答一下这个题目吗?感谢您